What Is The Evergreen Portfolio Model? And Should You Use It

What Is The Evergreen Portfolio Model? And Should You Use It

The Evergreen Portfolio Model generates income from investments indefinitely without selling the underlying assets. Learn how the Three Pillars architecture replaces the outdated 4% rule and why ultra-wealthy families have used this approach for generations.

The Evergreen Portfolio Model generates income from investments indefinitely without selling the underlying assets. Learn how the Three Pillars architecture replaces the outdated 4% rule and why ultra-wealthy families have used this approach for generations.

by

Christopher Nelson

Key Takeaways

The Evergreen Portfolio Model generates enough income from investments to live on indefinitely without selling the underlying assets

Traditional drawdown portfolios (the 4% rule) deplete principal over time, creating a death spiral accelerated by sequence of returns risk

Evergreen portfolios use Three Pillars: Capital Preservation (3-4%), Income (6-10%), and Growth (10-15%). Each dollar has a specific job.

Ultra-wealthy families allocate up to 50% to alternatives: private equity, real estate, private credit. Assets that can generate income, appreciation, or both.

The same principles that preserve $500M dynasties apply to $5M portfolios. The difference is execution scale, not architecture.

With traditional advisors charging 1% AUM, the "4% rule" is really 3% net to you. You're paying someone to manage the decline.

What Is the Evergreen Portfolio Model?

The Evergreen Portfolio Model is a portfolio architecture that generates income indefinitely without selling the underlying assets.

The name comes from evergreen trees. They don't lose their leaves in winter. They stay green through all seasons. An Evergreen Portfolio stays intact through all market conditions, generating income year-round while the principal continues growing.

This is fundamentally different from how most people think about wealth.

The traditional model says: accumulate assets during your working years, then gradually sell them to fund retirement. Hope the pile lasts longer than you do.

The Evergreen model says: build a portfolio that produces income. Live on the distributions. Let the principal compound indefinitely, for you and for the next generation.

One depletes while the other compounds.

Two Ways to Design a Portfolio

Before choosing investments, you need to choose an architecture. This design decision shapes everything that follows.

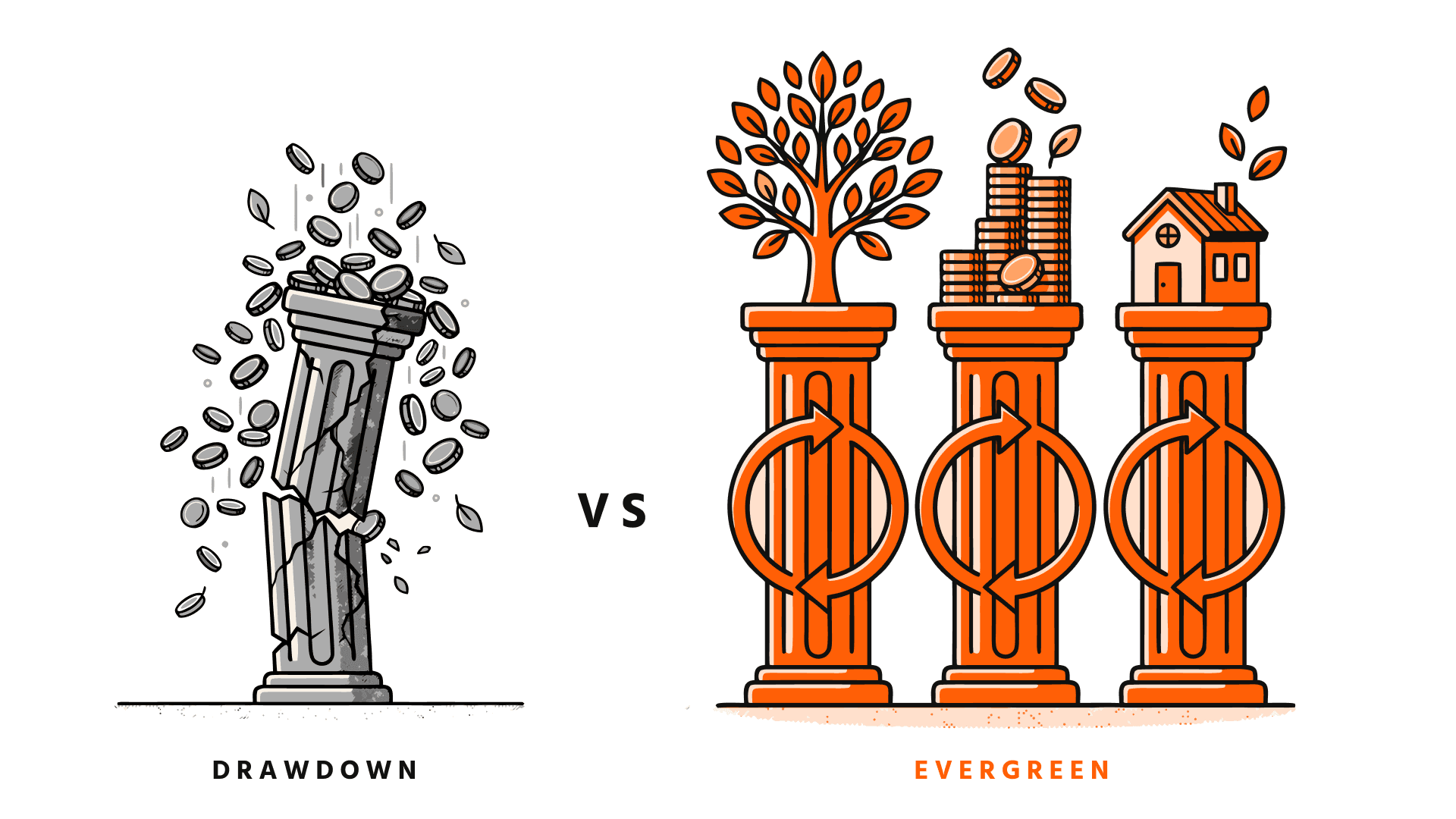

The Drawdown Architecture: Empty the Warehouse

This is what 95% of financial advisors recommend:

Save money during working years

Store wealth in a 60/40 portfolio

Withdraw 4% annually in retirement

Hope the money lasts 30 years

Goal: Don't die broke

The drawdown architecture treats wealth as a storage problem. You're filling a warehouse during your career, then emptying it until you die. Success means the warehouse isn't empty when you're gone.

The Evergreen Architecture: Harvest the Orchard

This is how ultra-wealthy families have structured portfolios for generations:

Build income-generating assets

Live on distributions, not principal

Preserve and grow the underlying capital

Pass the system to the next generation

Goal: Create perpetual wealth

The Evergreen architecture treats wealth as a production problem. You're planting an orchard, not filling a warehouse. Success means the orchard produces fruit indefinitely, and you pass the orchard down. Not an empty shed.

The question isn't "How much do I need to retire?"

It's "How much income can my portfolio generate without shrinking?"

This is the model that we follow inside of WealthOps.

Why Drawdown Portfolios Fail

The 4% rule has been the cornerstone of retirement planning since William Bengen's 1994 study. The idea: withdraw 4% of your portfolio annually (adjusted for inflation), and you probably won't run out of money over 30 years.

Three problems with this approach.

The Death Spiral: Sequence of Returns Risk

Research shows that 77% of your retirement outcome depends on returns in the first 10 years. Early losses are devastating.

When you withdraw during a down market, you're selling assets at the bottom. That locks in losses permanently. Your smaller portfolio then generates smaller returns, even when markets recover. You need to sell more to maintain the same income. The cycle accelerates.

This is the death spiral of drawdown portfolios.

Morningstar research confirms: if you experience poor returns in the first five years of retirement, your risk of depleting savings skyrockets. The 4% rule assumes average returns. Reality delivers sequence, and sequence matters more than average.

The 4% Rule Isn't 4% Anymore

Morningstar's 2024 analysis now recommends a 3.7% safe withdrawal rate, down from 4%, due to higher equity valuations and lower expected returns. PGIM calls the 4% rule a "research simplification" that doesn't account for real-world spending flexibility.

The "safe" number keeps declining as researchers stress-test the model against actual market conditions.

Your Advisor Takes a Cut First

Most people miss the fine print: the 4% rule assumes you keep all 4%.

If you're paying a traditional advisor 1% AUM (assets under management), you're not withdrawing 4%. You're withdrawing 5%. Four percent for your lifestyle, 1% for your advisor.

On a $3M portfolio:

4% withdrawal = $120K for you

1% AUM fee = $30K for your advisor

Gross depletion rate = 5%, not 4%

Over 20 years, that 1% AUM fee compounds to $400K-$600K+ depending on portfolio growth. You're paying someone to help you deplete your wealth more slowly.

The incentives are misaligned. AUM advisors are rewarded for keeping assets under management, not for building income streams that could reduce your dependence on the portfolio principal.

The Three Pillars: Every Dollar Has a Job

An Evergreen Portfolio assigns every dollar a specific job. Instead of mixing everything into a 60/40 blend and hoping for the best, you build three distinct pillars, each with a clear purpose.

Pillar | Purpose | Target Return | Role |

|---|---|---|---|

Capital Preservation | Protect from crashes | 3-4% | Shock absorber and liquidity |

Income | Fund your lifestyle | 6-10% | Cash flow without selling assets |

Growth | Build for next generation | 10-15% | Long-term compounding |

Capital Preservation: Your Shock Absorber

Capital Preservation assets protect purchasing power and provide liquidity when opportunities appear or emergencies strike. Treasury bills, high-yield savings, short-term bonds.

Not exciting. Essential.

When markets crash 30%, your Capital Preservation pillar stays stable and gives you the flexibility to buy assets on sale rather than sell them at a loss.

Target return: 3-4%. The goal isn't growth. It's stability and access.

Income: Your Cash Machine

Income assets generate regular distributions without requiring you to sell anything. Real estate syndications, private credit funds, REITs, dividend-paying alternatives.

This is the engine of the Evergreen model. While traditional portfolios generate 1-3% dividend yield, income-focused assets in private markets can generate 6-10% cash yield.

The math difference is significant. On $2M allocated to Income assets:

Traditional dividend yield (2%): $40K/year

Evergreen Income yield (8%): $160K/year

Same capital. 4X the cash flow.

That's the gap between hoping your money lasts and knowing it grows.

Growth: Your Legacy Builder

Growth assets focus on long-term appreciation. Growth stocks, private equity, venture capital. These don't produce income today. They compound wealth for tomorrow.

The Growth pillar is how your portfolio continues expanding even while the Income pillar pays your lifestyle. Target returns: 10-15% annually, though volatile.

The key insight: as your total wealth grows, you can decrease the Income percentage while increasing absolute income dollars, freeing up more capital for Growth.

At $2M, you might need 60% in Income to generate sufficient cash flow. At $10M, you might only need 35% in Income to generate even more dollars, which means 50%+ can compound in Growth.

This is how family offices build generational wealth. The architecture scales.

The Math That Changes Everything

Let's look at an example of a Traditional Portfolio. Let's assume $5M and a 60/40 stocks/bonds allocation:

S&P 500 dividend yield: ~1.3%

Bond yield: ~5%

Blended yield: ~2.5%

Annual income without selling: $125,000

To live on $200K, you must sell $75K of assets annually

Evergreen Portfolio ($5M, Three Pillars with 50% Income allocation):

Income pillar yield: 8%

Income from $2.5M Income allocation: $200,000

To live on $200K, you sell nothing

Same starting capital. One requires annual asset sales, depleting principal. One generates sufficient income, preserving principal.

Over 20 years, these paths diverge dramatically. The traditional portfolio shrinks while paying you. The Evergreen portfolio grows while paying you.

It's not a trick. It's asset selection and structure.

Who Actually Uses This?

This is how institutional wealth already operates.

Tiger 21, a peer network of ultra-high-net-worth investors managing $165+ billion collectively, publishes quarterly asset allocation reports. Their members allocate:

28% to private equity

26% to real estate

Up to 54% to alternatives that can generate income, appreciation, or both

Family offices globally show similar patterns. According to UBS and BlackRock research, alternatives represent 42-54% of family office portfolios, with private equity and real estate leading allocations.

The pattern is consistent: those managing $10M+ allocate heavily to alternative assets. Those managing $500K follow the 60/40 model their advisor recommends.

The difference isn't sophistication. The barrier has been access. Private investments historically required $1M+ minimums and institutional connections. That's changing. Accredited investors (most people with $1M+ net worth or $200K+ income) now have access to the same asset classes.

The question isn't "Can I access these investments?" anymore. It's "Do I understand how to structure them?"

Side-by-Side: Evergreen vs. Drawdown

Dimension | Drawdown Architecture | Evergreen Architecture |

|---|---|---|

Design | Store wealth, deplete over time | Generate income, compound indefinitely |

Goal | Don't run out of money | Build perpetual wealth |

Income Source | Sell assets | Collect distributions |

Principal Trajectory | Decreases over time | Stays stable or grows |

Sequence Risk | High. Early losses devastate. | Lower. Income continues regardless. |

Legacy | Hopefully something left | System transfers to next generation |

Your Role | Account holder | Portfolio CEO |

Frequently Asked Questions

Is the Evergreen Model right for everyone?

No. Evergreen portfolios require a CEO mindset, tolerance for illiquidity, and willingness to learn new asset classes. If you want completely passive, set-and-forget simplicity, the tradeoff is lower income and gradual depletion. You should choose the architecture that matches how you want to operate.

How much do I need to start building an Evergreen Portfolio?

The principles apply at any level, but practical access to private market income assets typically requires accredited investor status ($200K income or $1M net worth excluding primary residence). Most people with $1M+ can begin implementing Evergreen principles.

What about liquidity? Aren't these assets locked up?

Yes, Income assets like private real estate or credit funds often have 3-7 year hold periods. That illiquidity is part of why yields are higher. Your Capital Preservation pillar provides liquidity. Your Income pillar provides cash flow. You don't need to sell Income assets to access cash.

How is this different from dividend investing?

Dividend investing focuses on public market stocks paying 2-4% yields. Evergreen portfolios include private market assets yielding 6-10%+. The yield differential is 2-3X, which compounds to dramatically different outcomes over time. Many private Income assets also offer tax advantages (like depreciation) that dividend stocks don't.

Do I need to be an accredited investor?

For full implementation with private equity and real estate syndications, yes. But the Three Pillars architecture applies regardless. You can build Capital Preservation/Income/Growth allocations using public market equivalents (Treasury ETFs, REITs, index funds) while working toward accredited status.

The Bottom Line

The Evergreen Portfolio Model isn't a collection of investment picks. It's a portfolio architecture.

Drawdown portfolios treat wealth as a storage problem. Fill the warehouse, empty it slowly, hope it lasts.

Evergreen portfolios treat wealth as a production problem. Plant an orchard, harvest the fruit, pass down the trees.

Ultra-wealthy families figured this out generations ago. They allocate up to 50% to alternatives. Private equity, real estate, private credit. They live on distributions, not principal. They build systems that compound across generations.

The principles aren't secret. The access wasn't available. That's changing.

The Evergreen Portfolio Model is one component of how a Micro Family Office operates: systematic wealth architecture that generates income while preserving and growing capital.

If your goal is generational wealth, you need to stop depleting and start generating.

Key Takeaways

The Evergreen Portfolio Model generates enough income from investments to live on indefinitely without selling the underlying assets

Traditional drawdown portfolios (the 4% rule) deplete principal over time, creating a death spiral accelerated by sequence of returns risk

Evergreen portfolios use Three Pillars: Capital Preservation (3-4%), Income (6-10%), and Growth (10-15%). Each dollar has a specific job.

Ultra-wealthy families allocate up to 50% to alternatives: private equity, real estate, private credit. Assets that can generate income, appreciation, or both.

The same principles that preserve $500M dynasties apply to $5M portfolios. The difference is execution scale, not architecture.

With traditional advisors charging 1% AUM, the "4% rule" is really 3% net to you. You're paying someone to manage the decline.

What Is the Evergreen Portfolio Model?

The Evergreen Portfolio Model is a portfolio architecture that generates income indefinitely without selling the underlying assets.

The name comes from evergreen trees. They don't lose their leaves in winter. They stay green through all seasons. An Evergreen Portfolio stays intact through all market conditions, generating income year-round while the principal continues growing.

This is fundamentally different from how most people think about wealth.

The traditional model says: accumulate assets during your working years, then gradually sell them to fund retirement. Hope the pile lasts longer than you do.

The Evergreen model says: build a portfolio that produces income. Live on the distributions. Let the principal compound indefinitely, for you and for the next generation.

One depletes while the other compounds.

Two Ways to Design a Portfolio

Before choosing investments, you need to choose an architecture. This design decision shapes everything that follows.

The Drawdown Architecture: Empty the Warehouse

This is what 95% of financial advisors recommend:

Save money during working years

Store wealth in a 60/40 portfolio

Withdraw 4% annually in retirement

Hope the money lasts 30 years

Goal: Don't die broke

The drawdown architecture treats wealth as a storage problem. You're filling a warehouse during your career, then emptying it until you die. Success means the warehouse isn't empty when you're gone.

The Evergreen Architecture: Harvest the Orchard

This is how ultra-wealthy families have structured portfolios for generations:

Build income-generating assets

Live on distributions, not principal

Preserve and grow the underlying capital

Pass the system to the next generation

Goal: Create perpetual wealth

The Evergreen architecture treats wealth as a production problem. You're planting an orchard, not filling a warehouse. Success means the orchard produces fruit indefinitely, and you pass the orchard down. Not an empty shed.

The question isn't "How much do I need to retire?"

It's "How much income can my portfolio generate without shrinking?"

This is the model that we follow inside of WealthOps.

Why Drawdown Portfolios Fail

The 4% rule has been the cornerstone of retirement planning since William Bengen's 1994 study. The idea: withdraw 4% of your portfolio annually (adjusted for inflation), and you probably won't run out of money over 30 years.

Three problems with this approach.

The Death Spiral: Sequence of Returns Risk

Research shows that 77% of your retirement outcome depends on returns in the first 10 years. Early losses are devastating.

When you withdraw during a down market, you're selling assets at the bottom. That locks in losses permanently. Your smaller portfolio then generates smaller returns, even when markets recover. You need to sell more to maintain the same income. The cycle accelerates.

This is the death spiral of drawdown portfolios.

Morningstar research confirms: if you experience poor returns in the first five years of retirement, your risk of depleting savings skyrockets. The 4% rule assumes average returns. Reality delivers sequence, and sequence matters more than average.

The 4% Rule Isn't 4% Anymore

Morningstar's 2024 analysis now recommends a 3.7% safe withdrawal rate, down from 4%, due to higher equity valuations and lower expected returns. PGIM calls the 4% rule a "research simplification" that doesn't account for real-world spending flexibility.

The "safe" number keeps declining as researchers stress-test the model against actual market conditions.

Your Advisor Takes a Cut First

Most people miss the fine print: the 4% rule assumes you keep all 4%.

If you're paying a traditional advisor 1% AUM (assets under management), you're not withdrawing 4%. You're withdrawing 5%. Four percent for your lifestyle, 1% for your advisor.

On a $3M portfolio:

4% withdrawal = $120K for you

1% AUM fee = $30K for your advisor

Gross depletion rate = 5%, not 4%

Over 20 years, that 1% AUM fee compounds to $400K-$600K+ depending on portfolio growth. You're paying someone to help you deplete your wealth more slowly.

The incentives are misaligned. AUM advisors are rewarded for keeping assets under management, not for building income streams that could reduce your dependence on the portfolio principal.

The Three Pillars: Every Dollar Has a Job

An Evergreen Portfolio assigns every dollar a specific job. Instead of mixing everything into a 60/40 blend and hoping for the best, you build three distinct pillars, each with a clear purpose.

Pillar | Purpose | Target Return | Role |

|---|---|---|---|

Capital Preservation | Protect from crashes | 3-4% | Shock absorber and liquidity |

Income | Fund your lifestyle | 6-10% | Cash flow without selling assets |

Growth | Build for next generation | 10-15% | Long-term compounding |

Capital Preservation: Your Shock Absorber

Capital Preservation assets protect purchasing power and provide liquidity when opportunities appear or emergencies strike. Treasury bills, high-yield savings, short-term bonds.

Not exciting. Essential.

When markets crash 30%, your Capital Preservation pillar stays stable and gives you the flexibility to buy assets on sale rather than sell them at a loss.

Target return: 3-4%. The goal isn't growth. It's stability and access.

Income: Your Cash Machine

Income assets generate regular distributions without requiring you to sell anything. Real estate syndications, private credit funds, REITs, dividend-paying alternatives.

This is the engine of the Evergreen model. While traditional portfolios generate 1-3% dividend yield, income-focused assets in private markets can generate 6-10% cash yield.

The math difference is significant. On $2M allocated to Income assets:

Traditional dividend yield (2%): $40K/year

Evergreen Income yield (8%): $160K/year

Same capital. 4X the cash flow.

That's the gap between hoping your money lasts and knowing it grows.

Growth: Your Legacy Builder

Growth assets focus on long-term appreciation. Growth stocks, private equity, venture capital. These don't produce income today. They compound wealth for tomorrow.

The Growth pillar is how your portfolio continues expanding even while the Income pillar pays your lifestyle. Target returns: 10-15% annually, though volatile.

The key insight: as your total wealth grows, you can decrease the Income percentage while increasing absolute income dollars, freeing up more capital for Growth.

At $2M, you might need 60% in Income to generate sufficient cash flow. At $10M, you might only need 35% in Income to generate even more dollars, which means 50%+ can compound in Growth.

This is how family offices build generational wealth. The architecture scales.

The Math That Changes Everything

Let's look at an example of a Traditional Portfolio. Let's assume $5M and a 60/40 stocks/bonds allocation:

S&P 500 dividend yield: ~1.3%

Bond yield: ~5%

Blended yield: ~2.5%

Annual income without selling: $125,000

To live on $200K, you must sell $75K of assets annually

Evergreen Portfolio ($5M, Three Pillars with 50% Income allocation):

Income pillar yield: 8%

Income from $2.5M Income allocation: $200,000

To live on $200K, you sell nothing

Same starting capital. One requires annual asset sales, depleting principal. One generates sufficient income, preserving principal.

Over 20 years, these paths diverge dramatically. The traditional portfolio shrinks while paying you. The Evergreen portfolio grows while paying you.

It's not a trick. It's asset selection and structure.

Who Actually Uses This?

This is how institutional wealth already operates.

Tiger 21, a peer network of ultra-high-net-worth investors managing $165+ billion collectively, publishes quarterly asset allocation reports. Their members allocate:

28% to private equity

26% to real estate

Up to 54% to alternatives that can generate income, appreciation, or both

Family offices globally show similar patterns. According to UBS and BlackRock research, alternatives represent 42-54% of family office portfolios, with private equity and real estate leading allocations.

The pattern is consistent: those managing $10M+ allocate heavily to alternative assets. Those managing $500K follow the 60/40 model their advisor recommends.

The difference isn't sophistication. The barrier has been access. Private investments historically required $1M+ minimums and institutional connections. That's changing. Accredited investors (most people with $1M+ net worth or $200K+ income) now have access to the same asset classes.

The question isn't "Can I access these investments?" anymore. It's "Do I understand how to structure them?"

Side-by-Side: Evergreen vs. Drawdown

Dimension | Drawdown Architecture | Evergreen Architecture |

|---|---|---|

Design | Store wealth, deplete over time | Generate income, compound indefinitely |

Goal | Don't run out of money | Build perpetual wealth |

Income Source | Sell assets | Collect distributions |

Principal Trajectory | Decreases over time | Stays stable or grows |

Sequence Risk | High. Early losses devastate. | Lower. Income continues regardless. |

Legacy | Hopefully something left | System transfers to next generation |

Your Role | Account holder | Portfolio CEO |

Frequently Asked Questions

Is the Evergreen Model right for everyone?

No. Evergreen portfolios require a CEO mindset, tolerance for illiquidity, and willingness to learn new asset classes. If you want completely passive, set-and-forget simplicity, the tradeoff is lower income and gradual depletion. You should choose the architecture that matches how you want to operate.

How much do I need to start building an Evergreen Portfolio?

The principles apply at any level, but practical access to private market income assets typically requires accredited investor status ($200K income or $1M net worth excluding primary residence). Most people with $1M+ can begin implementing Evergreen principles.

What about liquidity? Aren't these assets locked up?

Yes, Income assets like private real estate or credit funds often have 3-7 year hold periods. That illiquidity is part of why yields are higher. Your Capital Preservation pillar provides liquidity. Your Income pillar provides cash flow. You don't need to sell Income assets to access cash.

How is this different from dividend investing?

Dividend investing focuses on public market stocks paying 2-4% yields. Evergreen portfolios include private market assets yielding 6-10%+. The yield differential is 2-3X, which compounds to dramatically different outcomes over time. Many private Income assets also offer tax advantages (like depreciation) that dividend stocks don't.

Do I need to be an accredited investor?

For full implementation with private equity and real estate syndications, yes. But the Three Pillars architecture applies regardless. You can build Capital Preservation/Income/Growth allocations using public market equivalents (Treasury ETFs, REITs, index funds) while working toward accredited status.

The Bottom Line

The Evergreen Portfolio Model isn't a collection of investment picks. It's a portfolio architecture.

Drawdown portfolios treat wealth as a storage problem. Fill the warehouse, empty it slowly, hope it lasts.

Evergreen portfolios treat wealth as a production problem. Plant an orchard, harvest the fruit, pass down the trees.

Ultra-wealthy families figured this out generations ago. They allocate up to 50% to alternatives. Private equity, real estate, private credit. They live on distributions, not principal. They build systems that compound across generations.

The principles aren't secret. The access wasn't available. That's changing.

The Evergreen Portfolio Model is one component of how a Micro Family Office operates: systematic wealth architecture that generates income while preserving and growing capital.

If your goal is generational wealth, you need to stop depleting and start generating.

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.