Everything You Need To Know About A Micro Family Office

Everything You Need To Know About A Micro Family Office

Stop managing accounts and start running a business. The Micro Family Office™ (MiFO) is the framework for investors with $1M–$30M to bridge the "service desert." Learn how to use the Two-Company Architecture to optimize taxes, protect assets, and become a Portfolio CEO.

Stop managing accounts and start running a business. The Micro Family Office™ (MiFO) is the framework for investors with $1M–$30M to bridge the "service desert." Learn how to use the Two-Company Architecture to optimize taxes, protect assets, and become a Portfolio CEO.

by

Christopher Nelson, former Tech Executive & Founder of WealthOps

Key Takeaways

A Micro Family Office™ (MiFO) is where you build a lean business around your wealth—giving it purpose, vision, and generational intention

It uses the same principles as single family offices and multi family offices but with scaled execution—technology and fractional advisors instead of full-time staff

Every MiFO has 7 core components: Vision, Structure, Protection, Process, Data, Advisory Partners, and Governance

The Two-Company Architecture—a Holding Company (The Vault) and Management Company (The Engine)—provides both asset protection and tax optimization

The skills you used to build your career—strategic planning, process building, vendor management—transfer directly to running a micro family office

The goal is to shift from passive investor to Portfolio CEO—setting strategy while experts execute

What Is a Micro Family Office?

A Micro Family Office™ (MiFO) is where you build a lean business around your wealth using the WealthOps framework.

Not a collection of accounts. Not a pile of statements from different institutions. A business—with purpose, vision, structure, and governance. A micro family office applies the same principles wealthy families have used for generations—systematic investment strategy, tax optimization, entity structuring, and coordinated advisory relationships—but with scaled execution appropriate for portfolios in the $1M to $30M range.

Unlike traditional family offices that require $100M+ in assets and seven-figure annual overhead, a micro family office leverages technology and fractional experts to deliver institutional-grade wealth management at a fraction of the cost.

Many people assume this adds complexity. The opposite is true.

If you've built a career in tech, finance, or business, you already have the skills. Strategic planning, systematic execution, vendor management, building processes—these are the same capabilities required to run a micro family office. The skills transfer immediately. What feels foreign at first becomes natural once you see the framework.

The difference between families who build lasting wealth and those who don't often comes down to one thing: infrastructure. A micro family office gives your wealth purpose, direction, and generational intention. It transforms a pile of assets into something that serves your family's mission for decades.

Why the Micro Family Office Is Gaining Traction

The micro family office concept is gaining traction—and the timing isn't coincidental.

The numbers tell the story:

$124 trillion is transferring between generations through 2048—the largest wealth transfer in history. Half of that ($62 trillion) is coming from high-net-worth and ultra-high-net-worth households. This isn't a future event. It's happening now.

23.8 million Americans are now millionaires—roughly 1 in 10 adults. The U.S. added over 560,000 new millionaires in 2024 alone. The population of people who need sophisticated wealth management is growing faster than the industry can serve them.

Family offices are multiplying. There are now over 8,000 single-family offices globally—a 31% increase since 2019. And 68% of all family offices were established after 2000. This isn't old money clinging to tradition. It's new wealth building infrastructure.

The demand for structured, intentional wealth management has never been higher. And for the $1M-$30M segment, the micro family office is emerging as the answer.

How Family Offices Created 150-Year Dynasties

Family offices aren't new.

The concept traces back centuries—European "major-domos" managed estates as early as the 6th century, and Medieval trusts preserved wealth across generations.

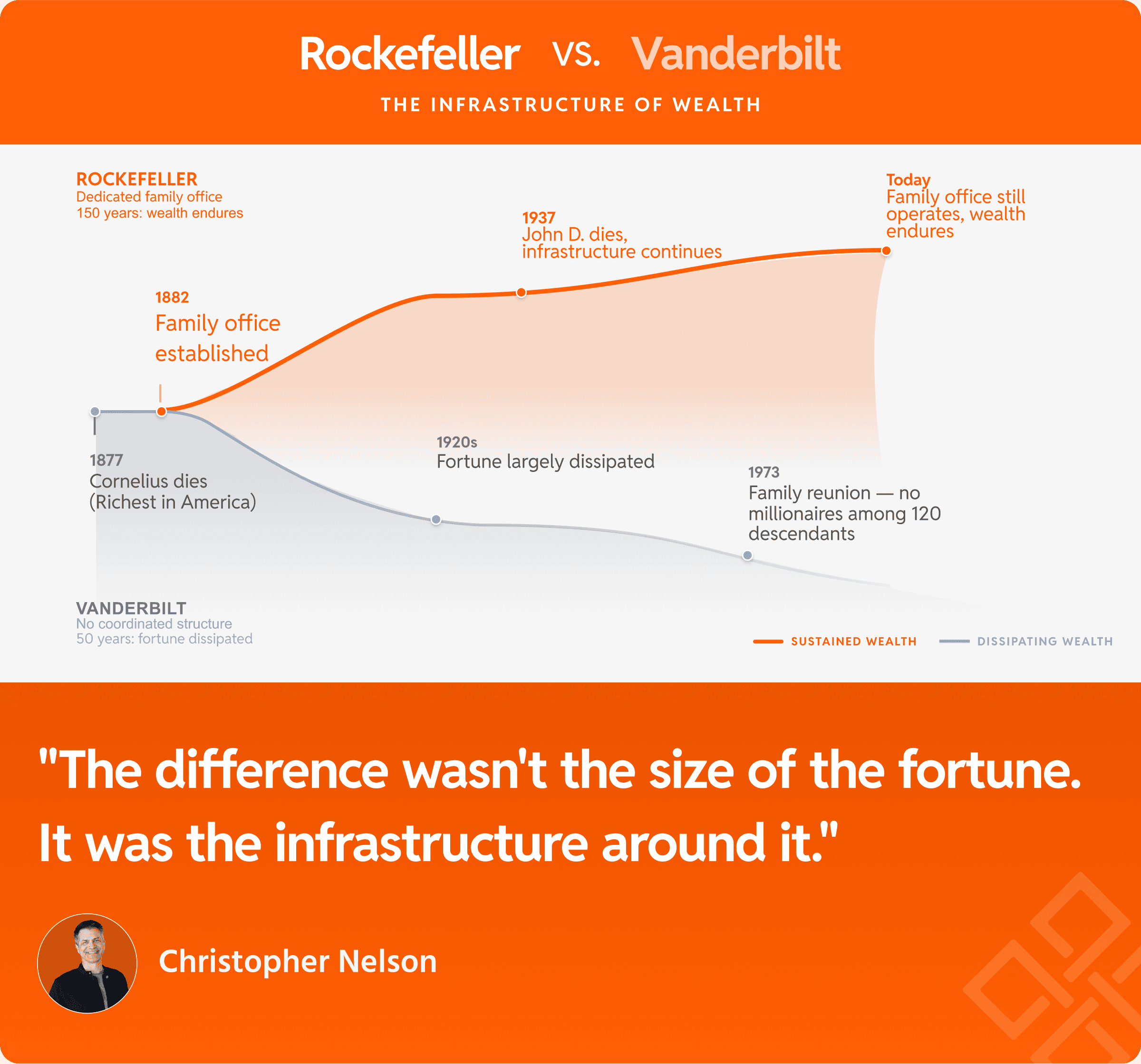

The modern model emerged during the Industrial Revolution. The Morgan family established their office in 1838. But John D. Rockefeller is widely credited with creating the first true single-family office in 1882—a dedicated structure to manage the family's vast holdings, investments, and legacy.

The Rockefeller vs. Vanderbilt Lesson

The contrast between the Rockefellers and the Vanderbilts tells you everything about why family offices matter.

Both families amassed enormous fortunes in the late 1800s. Cornelius Vanderbilt was the richest man in America when he died in 1877. But the Vanderbilts had no coordinated structure for managing or preserving their wealth. Within 50 years of Cornelius's death, the fortune had largely dissipated. By 1973, when 120 Vanderbilt descendants gathered for a family reunion, not one was a millionaire.

The Rockefellers took a different path.

John D. Rockefeller established a family office—a dedicated business to manage the family's wealth, investments, philanthropy, and legacy. That infrastructure created continuity. It gave the wealth purpose beyond any single generation. Today, nearly 150 years later, the Rockefeller family office still operates, and the family's wealth endures.

The difference wasn't the size of the fortune. It was the infrastructure around it.

A family office transforms wealth from something you have into something you run. It creates generational intention—a purpose, a mission, a system that outlasts any individual.

Why 68% of Family Offices Were Created After 2000

For over a century, this single family office infrastructure remained exclusive to the ultra-wealthy. You needed $100 million or more to justify the overhead.

That's changing.

68% of all family offices were established after 2000. Half have been created since the 2008 financial crisis. Technology, fractional services, and new financial products have made it possible to run family office infrastructure at a fraction of historical costs.

The Micro Family Office is the natural evolution: same principles, scaled execution. The Rockefeller model—adapted for the tech executive, the entrepreneur, the high-earning professional building their first significant wealth.

At WealthOps, we've developed a complete methodology for building and running a Micro Family Office—the frameworks, components, and systems that make this accessible to anyone in the $1M-$30M range. The concept is what we're explaining here. The methodology is how you actually build one.

Why High-Net-Worth Professionals Need a Micro Family Office

If you have $1M to $30M, you're in what we call the service desert.

You're too complex for retail financial services. A 60/40 portfolio and annual rebalancing doesn't address your equity compensation, concentrated stock positions, tax optimization opportunities, or estate planning needs.

But you're too small for traditional family offices. They won't take you as a client until you hit $30M, $50M, or $100M—depending on the firm.

The result? You're left navigating complex wealth decisions with advisors who aren't equipped to help, or you're doing it alone and hoping you don't miss something critical.

A micro family office closes this gap. It gives you the infrastructure to manage complexity systematically—without waiting until you're a hundred-millionaire to access it.

Micro Family Office vs. Traditional Family Office

Here's how micro family offices compare to traditional structures:

What Makes a Micro Family Office Different?

Technology replaces headcount. Instead of hiring a full-time bookkeeper, you use modern accounting software with quarterly CPA review. Instead of a dedicated analyst, you use portfolio tracking tools that aggregate data automatically.

Fractional experts replace full-time staff. You don't need a full-time tax strategist. You need a Certified Tax Planner for 10-20 hours per year. You don't need an in-house attorney. You need access to one when entity structuring or estate planning questions arise.

You remain the strategic decision-maker. In a traditional family office, you might delegate strategy entirely. In a micro family office, you're the Portfolio CEO—you set the vision, make the key decisions, and orchestrate the team. Advisors execute within your strategy, not the other way around.

The 7 Components of a Micro Family Office

Every functioning micro family office needs seven integrated components. Most people have one or two partially in place. The goal is building all seven—at the right level of complexity for your stage.

Vision Your wealth philosophy, legacy intentions, and decision-making framework. What is this money actually for? What does success look like in 10, 20, 50 years? What purpose does your wealth serve? Vision is what separates a micro family office from a collection of accounts. It's the "why" that guides every decision. Without vision, financial choices become reactive and ad hoc. With vision, you have a North Star—a generational intention that keeps everything aligned.

Structure Your portfolio architecture—how assets are categorized, allocated, and positioned for both growth and income. This isn't a pie chart from your advisor. It's an investment policy that guides every decision you make.

Protection Your entity architecture—the legal structures that hold, protect, and optimize your assets. This is where the Two-Company Architecture lives: a Holding Company for asset protection and a Management Company for active operations.

Process Your operational rhythms—bookkeeping, tax cadence, compliance tracking, document management. The systems that keep everything running without consuming your life.

Data Your performance tracking—the KPIs, dashboards, and metrics that tell you whether your wealth is actually growing, and where to focus attention.

Advisory Partners Your expert network—CPAs, attorneys, tax planners, investment managers. Not people who tell you what to do, but specialists who execute within your strategy.

Governance Your operating system as Portfolio CEO—meeting cadence, decision rights, review processes. How you actually run this thing week to week and year to year.

These seven components work together as a system. Vision informs Structure. Structure requires Protection. Protection needs Process. Everything generates Data. Advisory Partners execute within Governance.

When one component is missing, the others suffer. When all seven are in place, you have a wealth management machine.

The Two-Company Architecture: Protection + Optimization

One of the most powerful concepts in micro family office design is the Two-Company Architecture—separating your assets from your operations.

The Holding Company (The Vault)

Your Holding Company holds and protects assets. Think of it as The Vault.

What goes in:

Brokerage accounts

Private equity investments

Real estate (via subsidiary LLCs)

Startup investments

Limited partner positions

Primary purpose: Asset protection. Separating these assets from active operations—and from your personal life—creates a liability shield.

The Management Company (The Engine)

Your Management Company handles active operations. Think of it as The Engine.

What it does:

Investment research and deal analysis

Portfolio management activities

Contracts with service providers

Generates active income eligible for business deductions

Primary purpose: Tax optimization. Active trade or business status unlocks deductions and strategies unavailable to passive investors.

Why Separation Matters

If someone sues you personally, your Holding Company assets are protected. If something goes wrong in an active deal, it doesn't contaminate your broader portfolio.

Different jobs. Different entities. Same you running both.

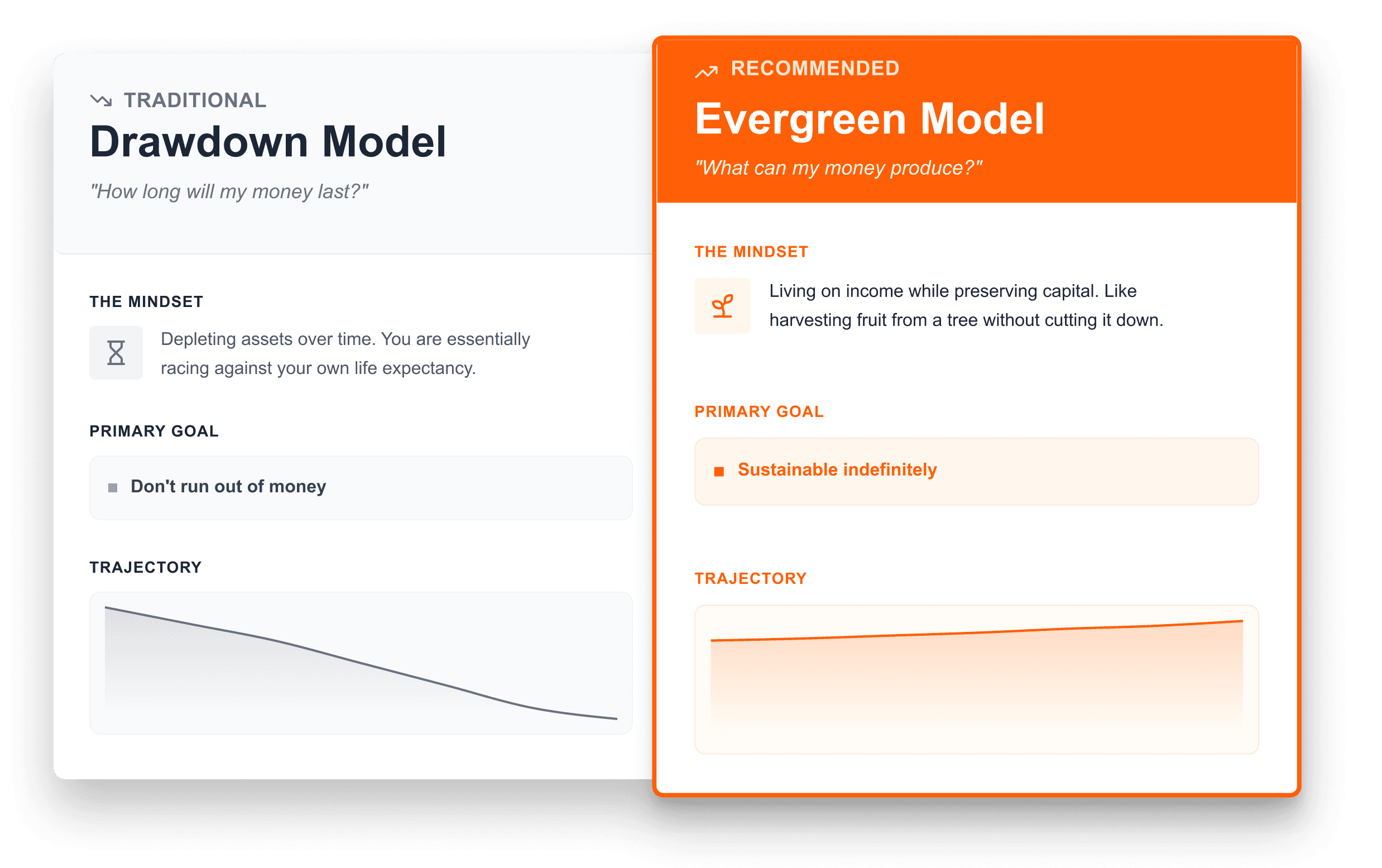

Evergreen vs. Drawdown: A Different Way to Think About Your Portfolio

Traditional retirement planning is built on a drawdown model: accumulate assets, then spend them down over 30 years. The math assumes you'll deplete your portfolio by the time you die.

A micro family office operates on an Evergreen model: build a portfolio that generates income to sustain your lifestyle indefinitely. You don't deplete the principal. You live off what it produces.

The Evergreen model changes everything—how you invest, what you optimize for, and how you think about generational wealth.

When your portfolio income covers 100% of your lifestyle expenses, work becomes optional. That's financial independence. When it covers 120% or more, you have a sustainable buffer. That's Evergreen.

This isn't about having more money. It's about building a portfolio that works like a business—generating returns you can live on without selling the underlying assets.

How a Micro Family Office Unlocks Tax Strategies

One of the primary advantages of a micro family office is access to tax optimization strategies typically reserved for business owners and sophisticated investors.

When you run your wealth like a business—with proper entity structure, documentation, and advisory relationships—you unlock strategies unavailable to passive investors.

We call this the Deduction Stack—a progression of tax strategies across seven levels.

Level 1 includes basic business deductions most business owners already know.

Levels 4-7 is where effective tax rates can drop significantly—strategies that require specific entity structures, proper documentation, and qualified advisory relationships to implement correctly.

Here's the catch: you can't access higher levels until you've built the infrastructure. Tax optimization isn't a list of tricks—it's a progression that requires the right foundation.

This is why the 7 components work as a connected system. Protection (entities) enables Process (documentation) which supports Advisory Partners (qualified relationships) which unlocks the full Deduction Stack.

How a Micro Family Office Changes Your Role

Building a micro family office isn't about becoming a financial expert. It's about becoming a Portfolio CEO.

The skills that built your wealth—operational thinking, systematic execution, strategic planning—are exactly what you need to manage it.

You don't need to analyze derivatives or read 10-Ks. You need to build infrastructure, coordinate a team, and make decisions.

You already know how to do that.

If you've ever managed a product roadmap, led a team, or built processes at scale, you have the foundation. Running a micro family office isn't learning something new—it's applying what you already know to a different domain.

The transition feels natural because it is.

Who Should Build a Micro Family Office?

A micro family office makes sense if you:

Have $1M-$30M in investable assets (or are on a clear path to get there)

Feel like traditional financial advice doesn't fit your situation

Want to be involved in strategy without doing all the execution yourself

Are a high-earning professional, entrepreneur, or tech executive

Have equity compensation (RSUs, ISOs, stock options) that requires coordination

Care about building generational wealth, not just retirement income

A micro family office may NOT be right if you:

Want someone else to handle everything with no involvement from you

Have $100M+ or less than $1M investable net worth

Don't want to learn new systems or frameworks

Prefer to keep finances completely separate from business thinking

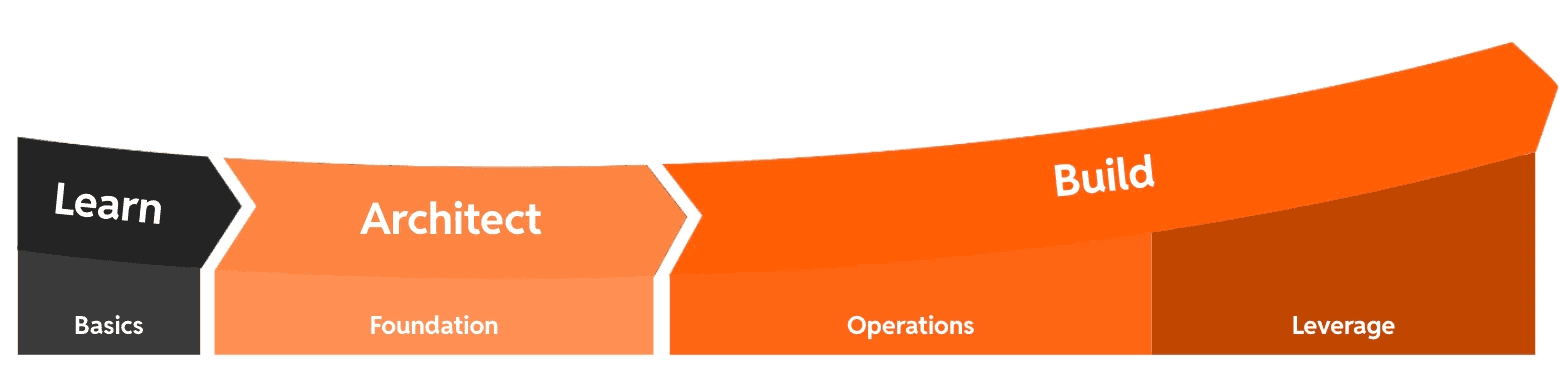

How to Start a Micro Family Office

Building a micro family office happens in phases:

Phase 1: LEARN

Understand the principles wealthy families use. See why traditional advice fails for your situation. Learn what a micro family office actually is and what it requires.

Phase 2: ARCHITECT

Design your vision, portfolio structure, and investment policy. Create the strategic foundation before building infrastructure.

Phase 3: BUILD

Implement the infrastructure—Protection (entities), Process (systems), Data (tracking), Advisory Partners (team), and Governance (operations). Each component is customized to your current stage.

The output is a complete implementation roadmap tailored to where you are today—not where you might be in ten years.

Frequently Asked Questions

What net worth do you need for a family office? Traditional single-family offices typically require $100M+ in assets. Multi-family offices start around $30M. A micro family office is designed specifically for the $1M-$30M range—using technology and fractional advisors to deliver similar capabilities at lower cost.

What's the difference between a family office and a wealth manager? A wealth manager typically focuses on investment management—building and managing your portfolio. A family office (including a micro family office) coordinates all aspects of wealth: investments, tax strategy, entity structure, estate planning, risk management, and governance. It's comprehensive infrastructure, not a single service.

Can I set up my own family office? Yes. A micro family office is specifically designed to be owner-operated. You serve as the Portfolio CEO, coordinating fractional advisors and technology rather than hiring full-time staff. You need to learn the frameworks and build the infrastructure, but you don't need to be a financial expert.

How is a micro family office different from DIY investing? DIY investing typically means managing your own portfolio. A micro family office is business infrastructure—it includes investment strategy but also entity structure, tax optimization, operational systems, advisory relationships, and governance. It's the difference between trading stocks and running a wealth management business.

Do I need a lot of money to start a micro family office? You can begin building micro family office infrastructure with $1M in investable assets. The key is matching your infrastructure complexity to your current stage. Start where you are and build progressively.

Is a micro family office worth it? For most people in the $1M-$30M range, the tax savings and investment optimization a micro family office generates exceeds the cost of building it. But the real value isn't just financial—it's the peace of mind that comes from running your wealth systematically instead of reactively.

What is WealthOps? WealthOps is an education company—not a financial advisor, not an investment firm. We don't sell investment products or manage money. We provide MBA-level education for first-generation high-net-worth individuals who want to learn how to manage their wealth with confidence and clarity. Our curriculum teaches the frameworks and systems for building a Micro Family Office—so you can run your wealth like a business, with the knowledge to make informed decisions and the infrastructure to execute them.

The Bottom Line

A micro family office gives you the infrastructure to manage $1M-$30M the way wealthy families manage $100M+: systematically, tax-efficiently, and with clear strategic vision.

More than that, it gives your wealth purpose. A mission. Generational intention. The Rockefellers didn't just accumulate money—they built a system to steward it across generations. That's the difference between wealth that dissipates and wealth that endures.

You're not waiting for permission. You're not hoping your advisor figures it out. You're building a business around your wealth—using skills you already possess.

Same principles. Scaled execution.

Let's keep building.

Key Takeaways

A Micro Family Office™ (MiFO) is where you build a lean business around your wealth—giving it purpose, vision, and generational intention

It uses the same principles as single family offices and multi family offices but with scaled execution—technology and fractional advisors instead of full-time staff

Every MiFO has 7 core components: Vision, Structure, Protection, Process, Data, Advisory Partners, and Governance

The Two-Company Architecture—a Holding Company (The Vault) and Management Company (The Engine)—provides both asset protection and tax optimization

The skills you used to build your career—strategic planning, process building, vendor management—transfer directly to running a micro family office

The goal is to shift from passive investor to Portfolio CEO—setting strategy while experts execute

What Is a Micro Family Office?

A Micro Family Office™ (MiFO) is where you build a lean business around your wealth using the WealthOps framework.

Not a collection of accounts. Not a pile of statements from different institutions. A business—with purpose, vision, structure, and governance. A micro family office applies the same principles wealthy families have used for generations—systematic investment strategy, tax optimization, entity structuring, and coordinated advisory relationships—but with scaled execution appropriate for portfolios in the $1M to $30M range.

Unlike traditional family offices that require $100M+ in assets and seven-figure annual overhead, a micro family office leverages technology and fractional experts to deliver institutional-grade wealth management at a fraction of the cost.

Many people assume this adds complexity. The opposite is true.

If you've built a career in tech, finance, or business, you already have the skills. Strategic planning, systematic execution, vendor management, building processes—these are the same capabilities required to run a micro family office. The skills transfer immediately. What feels foreign at first becomes natural once you see the framework.

The difference between families who build lasting wealth and those who don't often comes down to one thing: infrastructure. A micro family office gives your wealth purpose, direction, and generational intention. It transforms a pile of assets into something that serves your family's mission for decades.

Why the Micro Family Office Is Gaining Traction

The micro family office concept is gaining traction—and the timing isn't coincidental.

The numbers tell the story:

$124 trillion is transferring between generations through 2048—the largest wealth transfer in history. Half of that ($62 trillion) is coming from high-net-worth and ultra-high-net-worth households. This isn't a future event. It's happening now.

23.8 million Americans are now millionaires—roughly 1 in 10 adults. The U.S. added over 560,000 new millionaires in 2024 alone. The population of people who need sophisticated wealth management is growing faster than the industry can serve them.

Family offices are multiplying. There are now over 8,000 single-family offices globally—a 31% increase since 2019. And 68% of all family offices were established after 2000. This isn't old money clinging to tradition. It's new wealth building infrastructure.

The demand for structured, intentional wealth management has never been higher. And for the $1M-$30M segment, the micro family office is emerging as the answer.

How Family Offices Created 150-Year Dynasties

Family offices aren't new.

The concept traces back centuries—European "major-domos" managed estates as early as the 6th century, and Medieval trusts preserved wealth across generations.

The modern model emerged during the Industrial Revolution. The Morgan family established their office in 1838. But John D. Rockefeller is widely credited with creating the first true single-family office in 1882—a dedicated structure to manage the family's vast holdings, investments, and legacy.

The Rockefeller vs. Vanderbilt Lesson

The contrast between the Rockefellers and the Vanderbilts tells you everything about why family offices matter.

Both families amassed enormous fortunes in the late 1800s. Cornelius Vanderbilt was the richest man in America when he died in 1877. But the Vanderbilts had no coordinated structure for managing or preserving their wealth. Within 50 years of Cornelius's death, the fortune had largely dissipated. By 1973, when 120 Vanderbilt descendants gathered for a family reunion, not one was a millionaire.

The Rockefellers took a different path.

John D. Rockefeller established a family office—a dedicated business to manage the family's wealth, investments, philanthropy, and legacy. That infrastructure created continuity. It gave the wealth purpose beyond any single generation. Today, nearly 150 years later, the Rockefeller family office still operates, and the family's wealth endures.

The difference wasn't the size of the fortune. It was the infrastructure around it.

A family office transforms wealth from something you have into something you run. It creates generational intention—a purpose, a mission, a system that outlasts any individual.

Why 68% of Family Offices Were Created After 2000

For over a century, this single family office infrastructure remained exclusive to the ultra-wealthy. You needed $100 million or more to justify the overhead.

That's changing.

68% of all family offices were established after 2000. Half have been created since the 2008 financial crisis. Technology, fractional services, and new financial products have made it possible to run family office infrastructure at a fraction of historical costs.

The Micro Family Office is the natural evolution: same principles, scaled execution. The Rockefeller model—adapted for the tech executive, the entrepreneur, the high-earning professional building their first significant wealth.

At WealthOps, we've developed a complete methodology for building and running a Micro Family Office—the frameworks, components, and systems that make this accessible to anyone in the $1M-$30M range. The concept is what we're explaining here. The methodology is how you actually build one.

Why High-Net-Worth Professionals Need a Micro Family Office

If you have $1M to $30M, you're in what we call the service desert.

You're too complex for retail financial services. A 60/40 portfolio and annual rebalancing doesn't address your equity compensation, concentrated stock positions, tax optimization opportunities, or estate planning needs.

But you're too small for traditional family offices. They won't take you as a client until you hit $30M, $50M, or $100M—depending on the firm.

The result? You're left navigating complex wealth decisions with advisors who aren't equipped to help, or you're doing it alone and hoping you don't miss something critical.

A micro family office closes this gap. It gives you the infrastructure to manage complexity systematically—without waiting until you're a hundred-millionaire to access it.

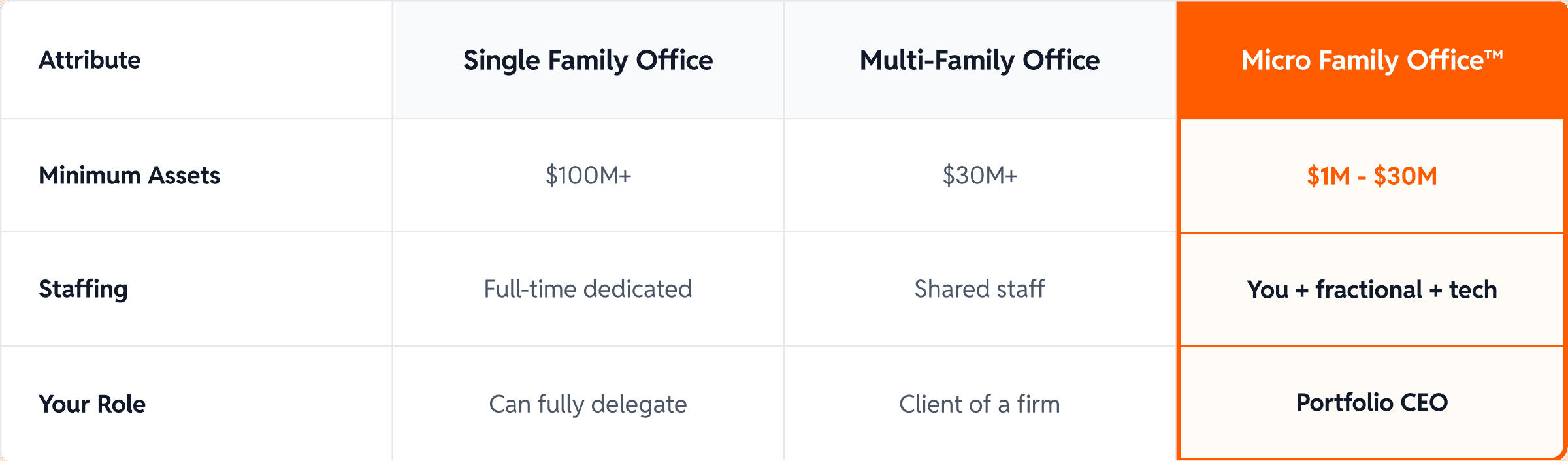

Micro Family Office vs. Traditional Family Office

Here's how micro family offices compare to traditional structures:

What Makes a Micro Family Office Different?

Technology replaces headcount. Instead of hiring a full-time bookkeeper, you use modern accounting software with quarterly CPA review. Instead of a dedicated analyst, you use portfolio tracking tools that aggregate data automatically.

Fractional experts replace full-time staff. You don't need a full-time tax strategist. You need a Certified Tax Planner for 10-20 hours per year. You don't need an in-house attorney. You need access to one when entity structuring or estate planning questions arise.

You remain the strategic decision-maker. In a traditional family office, you might delegate strategy entirely. In a micro family office, you're the Portfolio CEO—you set the vision, make the key decisions, and orchestrate the team. Advisors execute within your strategy, not the other way around.

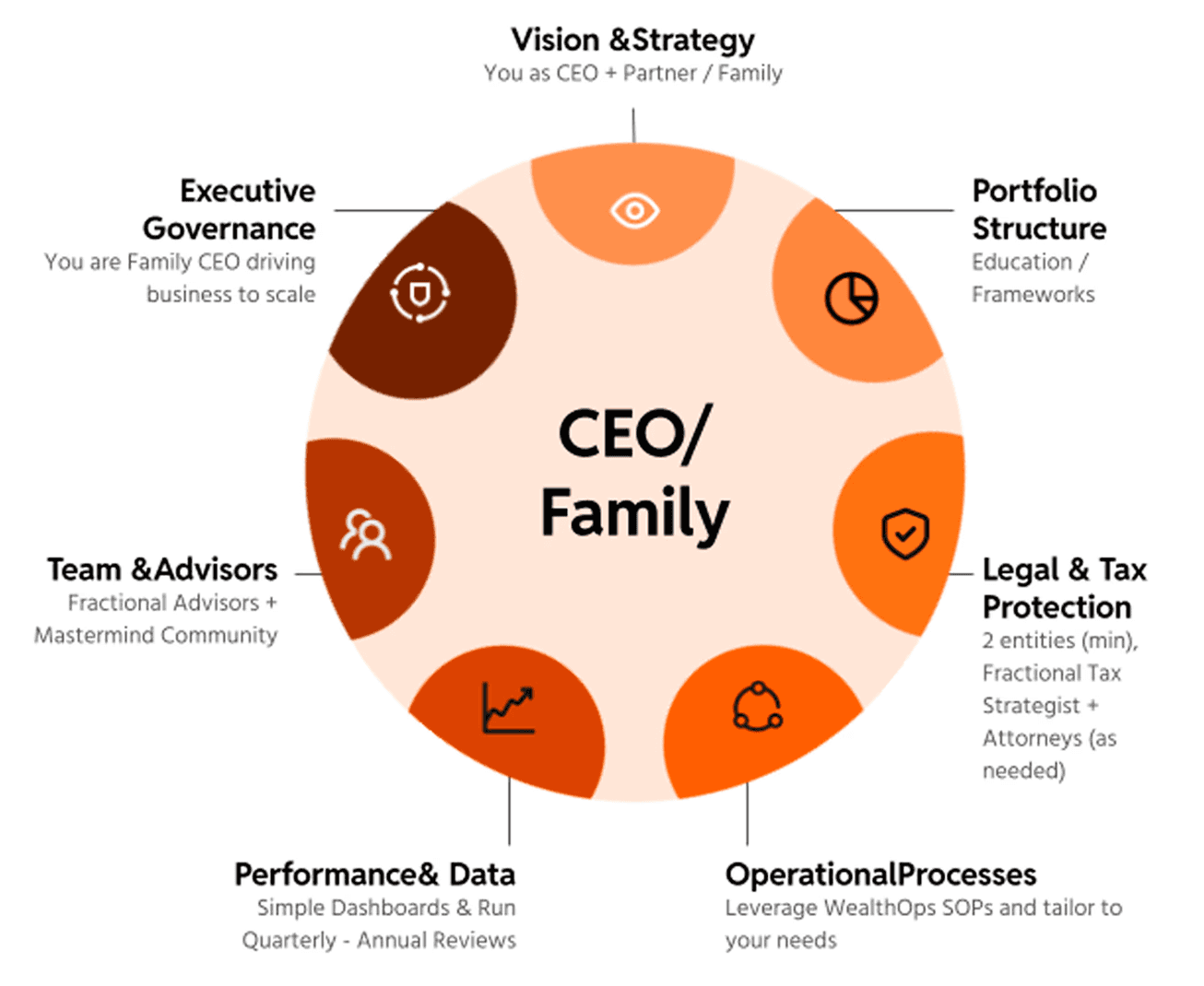

The 7 Components of a Micro Family Office

Every functioning micro family office needs seven integrated components. Most people have one or two partially in place. The goal is building all seven—at the right level of complexity for your stage.

Vision Your wealth philosophy, legacy intentions, and decision-making framework. What is this money actually for? What does success look like in 10, 20, 50 years? What purpose does your wealth serve? Vision is what separates a micro family office from a collection of accounts. It's the "why" that guides every decision. Without vision, financial choices become reactive and ad hoc. With vision, you have a North Star—a generational intention that keeps everything aligned.

Structure Your portfolio architecture—how assets are categorized, allocated, and positioned for both growth and income. This isn't a pie chart from your advisor. It's an investment policy that guides every decision you make.

Protection Your entity architecture—the legal structures that hold, protect, and optimize your assets. This is where the Two-Company Architecture lives: a Holding Company for asset protection and a Management Company for active operations.

Process Your operational rhythms—bookkeeping, tax cadence, compliance tracking, document management. The systems that keep everything running without consuming your life.

Data Your performance tracking—the KPIs, dashboards, and metrics that tell you whether your wealth is actually growing, and where to focus attention.

Advisory Partners Your expert network—CPAs, attorneys, tax planners, investment managers. Not people who tell you what to do, but specialists who execute within your strategy.

Governance Your operating system as Portfolio CEO—meeting cadence, decision rights, review processes. How you actually run this thing week to week and year to year.

These seven components work together as a system. Vision informs Structure. Structure requires Protection. Protection needs Process. Everything generates Data. Advisory Partners execute within Governance.

When one component is missing, the others suffer. When all seven are in place, you have a wealth management machine.

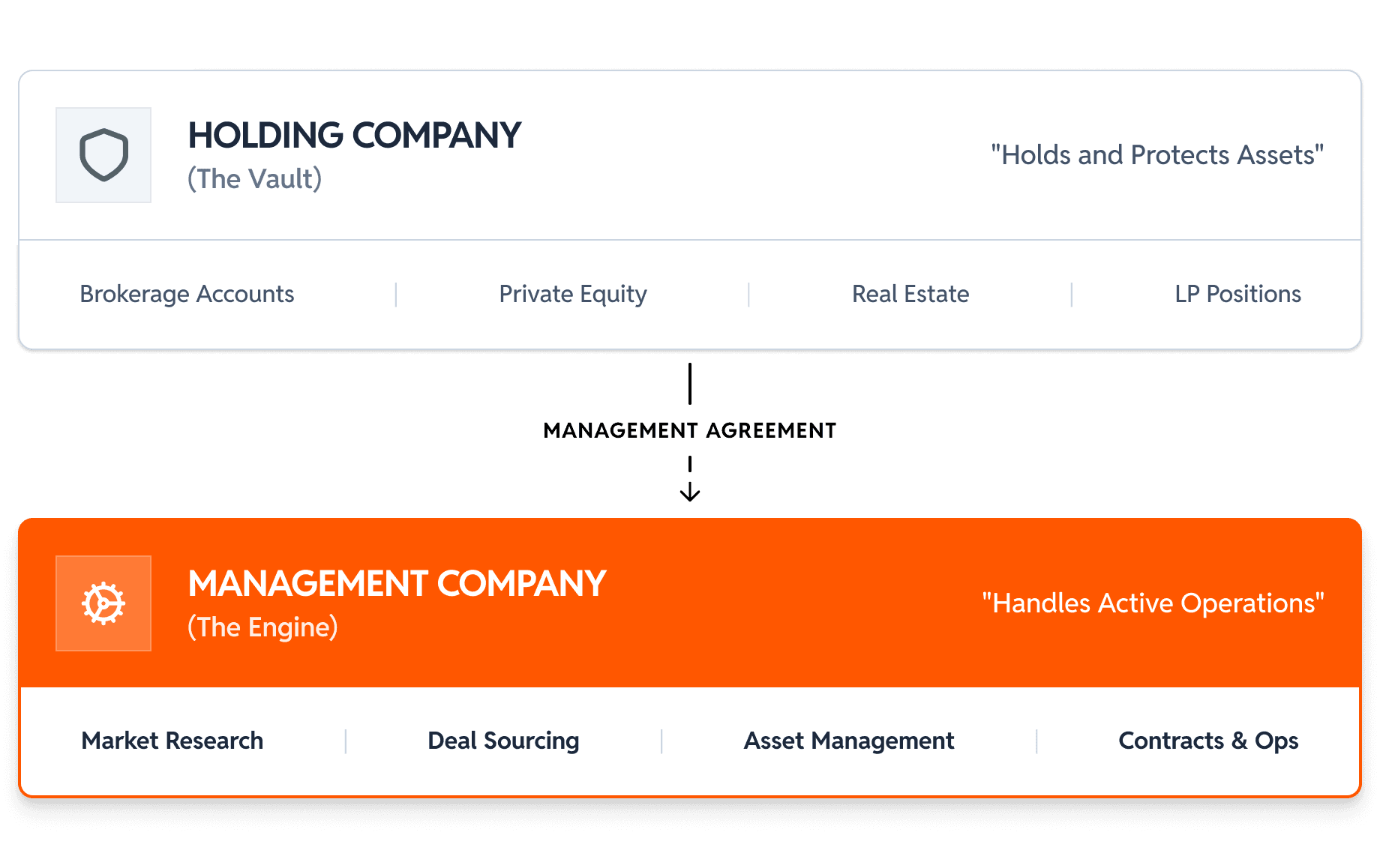

The Two-Company Architecture: Protection + Optimization

One of the most powerful concepts in micro family office design is the Two-Company Architecture—separating your assets from your operations.

The Holding Company (The Vault)

Your Holding Company holds and protects assets. Think of it as The Vault.

What goes in:

Brokerage accounts

Private equity investments

Real estate (via subsidiary LLCs)

Startup investments

Limited partner positions

Primary purpose: Asset protection. Separating these assets from active operations—and from your personal life—creates a liability shield.

The Management Company (The Engine)

Your Management Company handles active operations. Think of it as The Engine.

What it does:

Investment research and deal analysis

Portfolio management activities

Contracts with service providers

Generates active income eligible for business deductions

Primary purpose: Tax optimization. Active trade or business status unlocks deductions and strategies unavailable to passive investors.

Why Separation Matters

If someone sues you personally, your Holding Company assets are protected. If something goes wrong in an active deal, it doesn't contaminate your broader portfolio.

Different jobs. Different entities. Same you running both.

Evergreen vs. Drawdown: A Different Way to Think About Your Portfolio

Traditional retirement planning is built on a drawdown model: accumulate assets, then spend them down over 30 years. The math assumes you'll deplete your portfolio by the time you die.

A micro family office operates on an Evergreen model: build a portfolio that generates income to sustain your lifestyle indefinitely. You don't deplete the principal. You live off what it produces.

The Evergreen model changes everything—how you invest, what you optimize for, and how you think about generational wealth.

When your portfolio income covers 100% of your lifestyle expenses, work becomes optional. That's financial independence. When it covers 120% or more, you have a sustainable buffer. That's Evergreen.

This isn't about having more money. It's about building a portfolio that works like a business—generating returns you can live on without selling the underlying assets.

How a Micro Family Office Unlocks Tax Strategies

One of the primary advantages of a micro family office is access to tax optimization strategies typically reserved for business owners and sophisticated investors.

When you run your wealth like a business—with proper entity structure, documentation, and advisory relationships—you unlock strategies unavailable to passive investors.

We call this the Deduction Stack—a progression of tax strategies across seven levels.

Level 1 includes basic business deductions most business owners already know.

Levels 4-7 is where effective tax rates can drop significantly—strategies that require specific entity structures, proper documentation, and qualified advisory relationships to implement correctly.

Here's the catch: you can't access higher levels until you've built the infrastructure. Tax optimization isn't a list of tricks—it's a progression that requires the right foundation.

This is why the 7 components work as a connected system. Protection (entities) enables Process (documentation) which supports Advisory Partners (qualified relationships) which unlocks the full Deduction Stack.

How a Micro Family Office Changes Your Role

Building a micro family office isn't about becoming a financial expert. It's about becoming a Portfolio CEO.

The skills that built your wealth—operational thinking, systematic execution, strategic planning—are exactly what you need to manage it.

You don't need to analyze derivatives or read 10-Ks. You need to build infrastructure, coordinate a team, and make decisions.

You already know how to do that.

If you've ever managed a product roadmap, led a team, or built processes at scale, you have the foundation. Running a micro family office isn't learning something new—it's applying what you already know to a different domain.

The transition feels natural because it is.

Who Should Build a Micro Family Office?

A micro family office makes sense if you:

Have $1M-$30M in investable assets (or are on a clear path to get there)

Feel like traditional financial advice doesn't fit your situation

Want to be involved in strategy without doing all the execution yourself

Are a high-earning professional, entrepreneur, or tech executive

Have equity compensation (RSUs, ISOs, stock options) that requires coordination

Care about building generational wealth, not just retirement income

A micro family office may NOT be right if you:

Want someone else to handle everything with no involvement from you

Have $100M+ or less than $1M investable net worth

Don't want to learn new systems or frameworks

Prefer to keep finances completely separate from business thinking

How to Start a Micro Family Office

Building a micro family office happens in phases:

Phase 1: LEARN

Understand the principles wealthy families use. See why traditional advice fails for your situation. Learn what a micro family office actually is and what it requires.

Phase 2: ARCHITECT

Design your vision, portfolio structure, and investment policy. Create the strategic foundation before building infrastructure.

Phase 3: BUILD

Implement the infrastructure—Protection (entities), Process (systems), Data (tracking), Advisory Partners (team), and Governance (operations). Each component is customized to your current stage.

The output is a complete implementation roadmap tailored to where you are today—not where you might be in ten years.

Frequently Asked Questions

What net worth do you need for a family office? Traditional single-family offices typically require $100M+ in assets. Multi-family offices start around $30M. A micro family office is designed specifically for the $1M-$30M range—using technology and fractional advisors to deliver similar capabilities at lower cost.

What's the difference between a family office and a wealth manager? A wealth manager typically focuses on investment management—building and managing your portfolio. A family office (including a micro family office) coordinates all aspects of wealth: investments, tax strategy, entity structure, estate planning, risk management, and governance. It's comprehensive infrastructure, not a single service.

Can I set up my own family office? Yes. A micro family office is specifically designed to be owner-operated. You serve as the Portfolio CEO, coordinating fractional advisors and technology rather than hiring full-time staff. You need to learn the frameworks and build the infrastructure, but you don't need to be a financial expert.

How is a micro family office different from DIY investing? DIY investing typically means managing your own portfolio. A micro family office is business infrastructure—it includes investment strategy but also entity structure, tax optimization, operational systems, advisory relationships, and governance. It's the difference between trading stocks and running a wealth management business.

Do I need a lot of money to start a micro family office? You can begin building micro family office infrastructure with $1M in investable assets. The key is matching your infrastructure complexity to your current stage. Start where you are and build progressively.

Is a micro family office worth it? For most people in the $1M-$30M range, the tax savings and investment optimization a micro family office generates exceeds the cost of building it. But the real value isn't just financial—it's the peace of mind that comes from running your wealth systematically instead of reactively.

What is WealthOps? WealthOps is an education company—not a financial advisor, not an investment firm. We don't sell investment products or manage money. We provide MBA-level education for first-generation high-net-worth individuals who want to learn how to manage their wealth with confidence and clarity. Our curriculum teaches the frameworks and systems for building a Micro Family Office—so you can run your wealth like a business, with the knowledge to make informed decisions and the infrastructure to execute them.

The Bottom Line

A micro family office gives you the infrastructure to manage $1M-$30M the way wealthy families manage $100M+: systematically, tax-efficiently, and with clear strategic vision.

More than that, it gives your wealth purpose. A mission. Generational intention. The Rockefellers didn't just accumulate money—they built a system to steward it across generations. That's the difference between wealth that dissipates and wealth that endures.

You're not waiting for permission. You're not hoping your advisor figures it out. You're building a business around your wealth—using skills you already possess.

Same principles. Scaled execution.

Let's keep building.

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.