What Is the Service Desert?

What Is the Service Desert?

The wealth management industry systematically underserves $1M-$30M investors. Learn why the Financial Service Desert exists and what you can do about it.

The wealth management industry systematically underserves $1M-$30M investors. Learn why the Financial Service Desert exists and what you can do about it.

by

Christopher Nelson

What Is the Financial Service Desert?

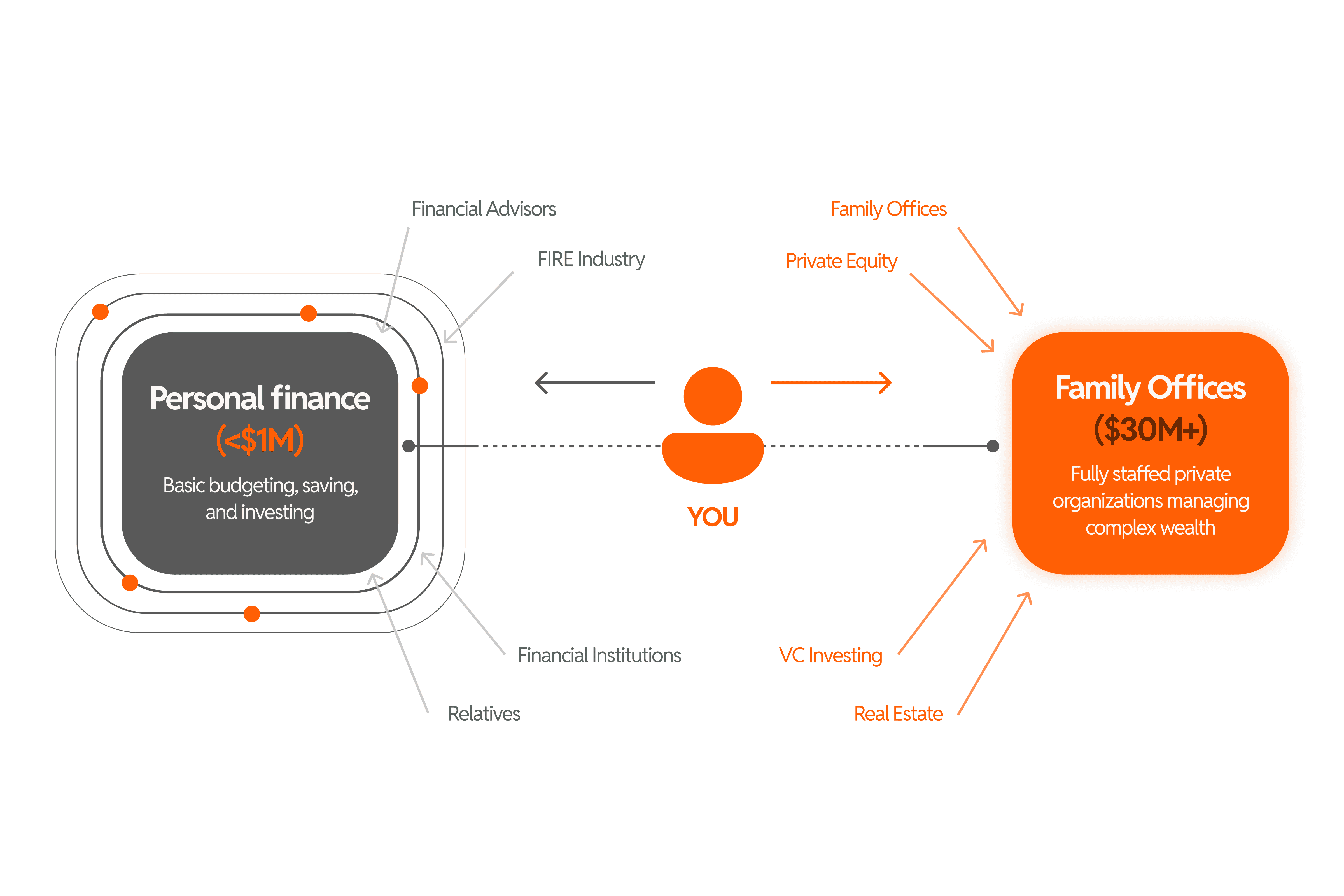

The Service Desert is the $1M-$30M wealth gap where no systematic solutions exist.

You're too complex for retail financial services. Robo-advisors can't handle equity compensation, alternative investments, or multi-entity tax strategy. Target-date funds weren't designed for someone building a real estate portfolio alongside their brokerage account.

You're too "small" for family office infrastructure. Single family offices require $100M minimum—some say $250M or more to justify the $1-2M annual operating cost. Multi-family offices set their floors at $25M-$100M and still treat you like a number.

The industry calls you "high net worth." Then it treats you like everyone else.

McKinsey defines the high-net-worth segment as $2M-$25M in investable assets. That's a massive range. And here's what the data shows: a $10M client paying $50,000 per year in advisory fees often receives identical treatment as a $2M client paying $16,000. Same templates. Same quarterly calls. Same recommendations.

You're paying three times as much for the same service.

TL;DR: The Service Desert is the $1M-$30M wealth gap where investors are too complex for retail services but too "small" for family office infrastructure. Despite paying $16K-$50K+ in fees annually, most receive identical template advice designed for retirement planning, not wealth building.

Why Does the Service Desert Miss What You Actually Want?

You didn't build $1M-$30M by being passive.

The wealth management industry assumes you need someone to "handle it for you." But you made this money by understanding how to build, evaluate opportunities, and make strategic decisions.

Now you want to apply that same mindset to your wealth.

The market is changing. Professionals with $1M-$30M aren't looking for someone to take over. They're looking for:

Control — Not blind delegation. You want to understand the strategy and own the decisions.

Strategic partnership — Not a relationship where moving capital outside the advisor's control feels like a betrayal.

Education to make more — Not gatekeeping disguised as "too risky for you."

This creates a fundamental mismatch. The traditional advisory model was built for a different client: someone nearing retirement who wants preservation. Someone who WANTS to delegate everything.

You're optimizing for growth. You want a partner, not a parent.

And the industry has no construct for that.

Here's why.

Why the Gap Exists

The Service Desert isn't a market failure. It's market design for a client that isn't you.

The Three Structural Failures:

The Service Desert exists because of three structural failures in the traditional wealth management model:

Training Mismatch: Advisors trained for retirement drawdown, not wealth building

Product Access Gap: Retail wrappers instead of institutional strategies

Incentive Misalignment: AUM model requires 100% dependency, no partial partnerships

Each failure has the same root cause: the model was designed for a different client.

Why Is Advisor Training Built for Drawdown, Not Growth?

Most financial advisors aren't trained to build wealth. They're trained for preservation and distribution.

What you want: Education on how to deploy capital strategically—PE deals, real estate syndications, business opportunities.

What they're trained for: 60/40 portfolios, target-date funds, and "don't outlive your money" drawdown strategies.

The origin of financial planning was selling products. That's still how many organizations operate today. You come in, you learn to sell. If you do well at sales, maybe at some point you get the opportunity to pursue your CFP certification and become an actual financial planner.

The result? There's a legal difference between advisors and salespeople. There's a standards difference. There's a training and education difference. But the industry doesn't discriminate in how those titles work. The person calling themselves your "wealth advisor" may have six weeks of product training, two weeks of sales training, and zero days on private equity, real estate syndication, or entity-based tax optimization.

Why? Because 65% of their clients are over 50, preparing for retirement. Their training is optimized for distribution, not accumulation. For preservation, not building.

You're trying to build. They're trained to help people draw down.

You're speaking different languages.

The model has no construct for: "Teach me how this works so I can make the decision" instead of "Let me handle this for you."

Why Don't You Get Access to Institutional Products?

What you want: Access to the same asset classes and deal flow that drive family office returns.

What you get: Retail wrappers of institutional strategies, with fees layered on top.

Here's where the gap becomes undeniable.

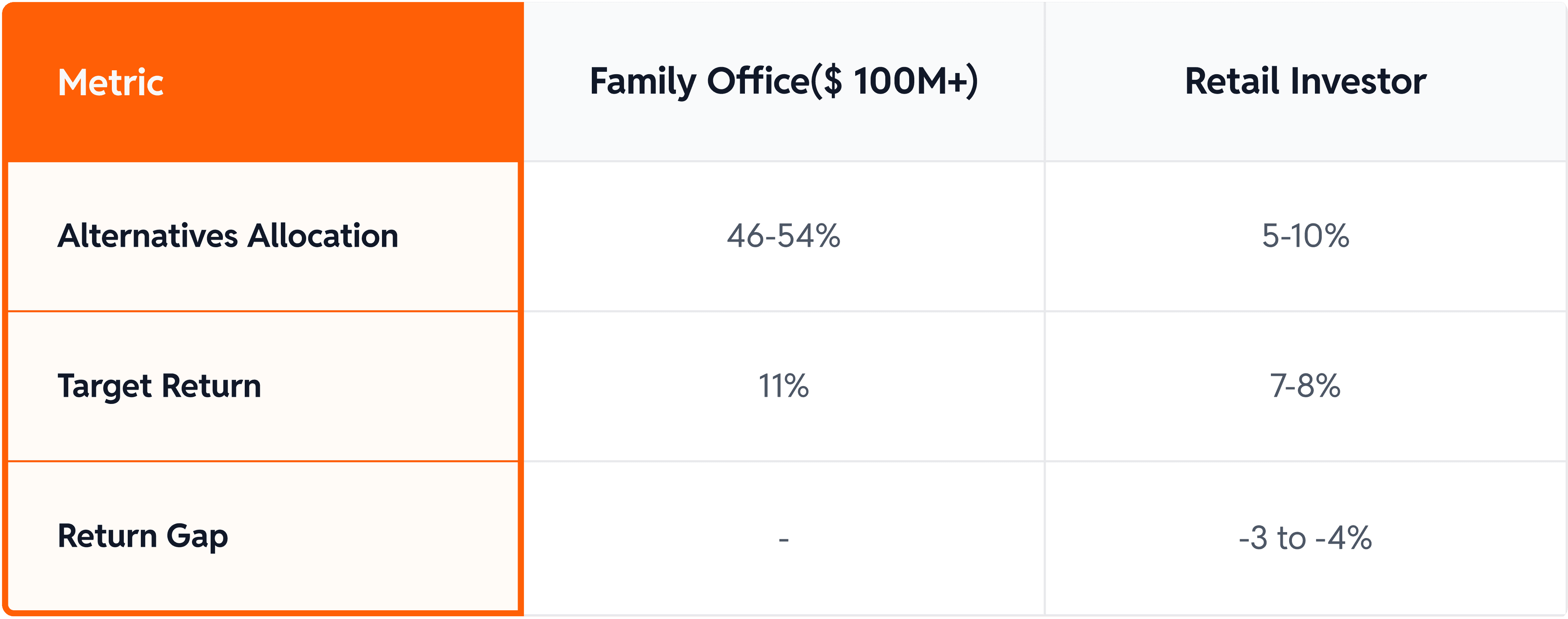

Family offices allocate 46-54% of their portfolios to alternative investments—private equity, venture capital, real estate, private credit. Their target return? 11%.

You? If you're lucky, you have 5-10% in alternatives, mostly through ETF wrappers or funds of funds with management fees layered on top. Your realistic target return? 7-8%.

That 3-4% difference compounds dramatically over decades.

But it gets worse. Private assets outperform public markets by 200-400 basis points annually. And 66% of family offices believe illiquidity—the very thing retail investors are told to avoid—actually boosts long-term returns.

The math is clear. The access is not.

Companies now stay private for 11 years before IPO. In the 1990s, it was six years. The value creation that used to happen in public markets—where you could participate—now happens before the company ever goes public. By the time you can buy, the biggest gains are already captured.

You're accredited. You legally qualify for private investments. But you get the retail versions of what actually builds wealth.

Why? The minimums.

Accredited investor ($1M net worth): Access to some private equity, but minimums of $250K-$1M per deal

Qualified Purchaser ($5M in investments): Access to better funds, 3(c)(7) structures, still limited deal flow

Family Office ($100M+): Co-investment alongside KKR, Blackstone, Bain Capital. Direct relationships with fund managers.

The investment opportunities that drive family office returns aren't available to you at the same scale, terms, or access points. You're playing on a different field.

The model has no construct for: Strategic allocation to alternatives alongside your managed account. Moving capital to a PE deal they can't access breaks their business model.

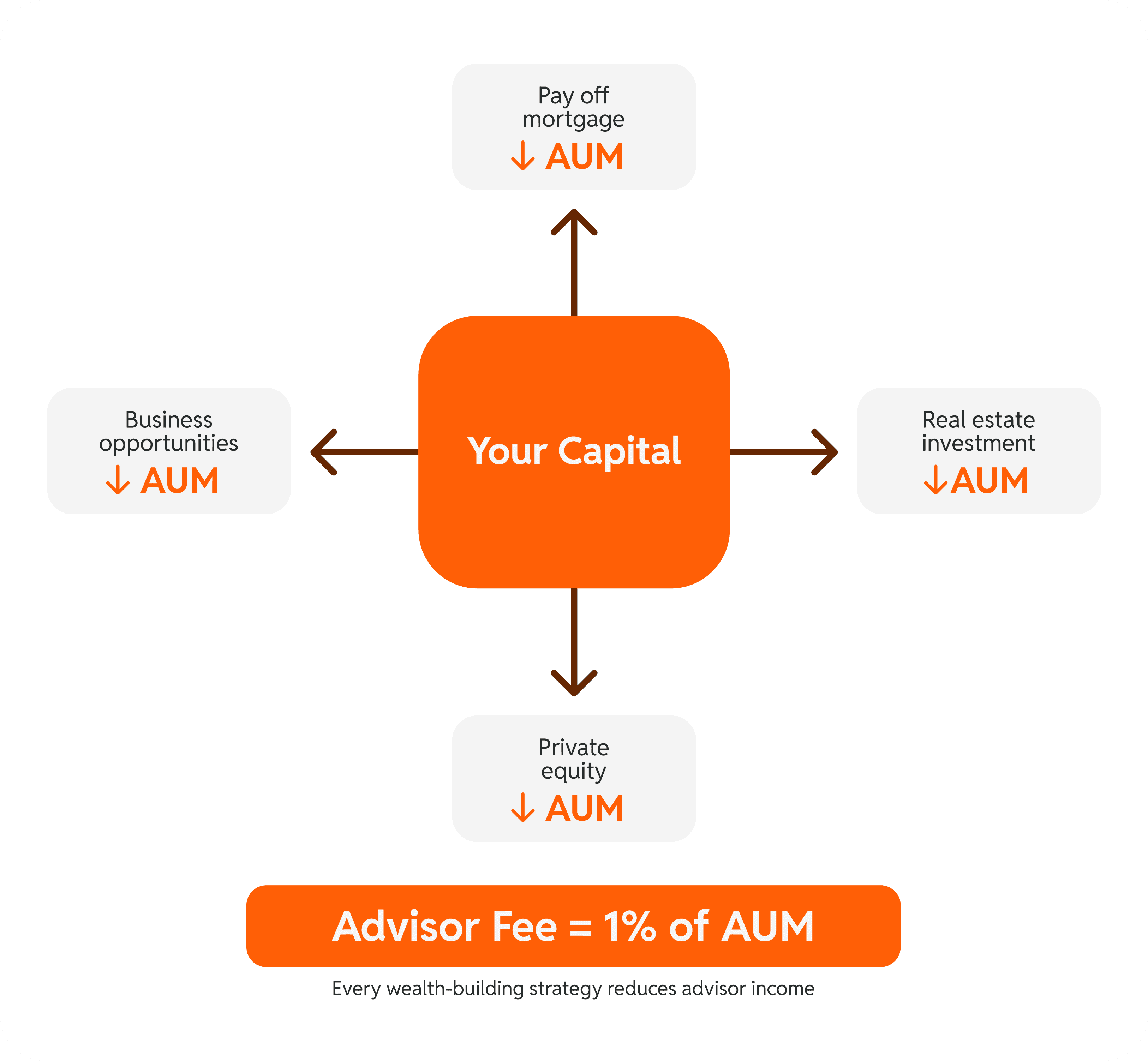

Why Do AUM Incentives Require Dependency?

What you want: A partner who helps you evaluate opportunities wherever they are—even if that means moving money outside their management.

What the model incentivizes: Keeping every dollar inside their AUM.

The AUM model—assets under management—creates structural conflicts that work against your interests.

Your advisor is paid a percentage of the assets they manage. Typically 1% annually. That means they're financially incentivized against anything that reduces your AUM:

Paying off your mortgage? Reduces AUM.

Investing in real estate they don't manage? Reduces AUM.

Moving money into private equity deals they can't access? Reduces AUM.

Using capital for business opportunities? Reduces AUM.

The strategies that build wealth often involve deploying capital outside your brokerage account. But every dollar that leaves is a dollar they stop earning on.

Fee-only doesn't mean conflict-free when the fee is tied to assets under management.

And as you move upmarket, seeking more sophisticated advice? The products get more complex—which means more fees layered in, more strings attached, more conflicts embedded. The exhaustion you feel isn't paranoia. Every interaction feels like a sales pitch because structurally, it is one.

The model has no construct for: Partial partnership. "I'll pay you for strategic advice and execution on X, but I'm also allocating to Y and Z on my own."

The business model requires 100% or nothing. You manage everything or you're not a client.

The Capacity Problem

Even good advisors can't solve this.

The average financial advisor manages 99-150 clients. That translates to roughly 4 hours per client per year—including all meetings, preparation, and follow-up.

Four hours.

For a $5M portfolio with equity compensation, real estate holdings, multiple entities, and complex tax considerations.

McKinsey projects the industry will face a shortage of roughly 100,000 advisors by 2034. The economics are pushing firms toward fewer clients with larger asset bases—not better service for anyone under $10M.

Rising costs mean rising minimums. Schwab raised their referral threshold from $500K to $2M. Private banks keep hiking their floors. The squeeze is on.

The result? You're either pushed down to robo-services that can't handle your complexity, or you're accepted as a client but served with template solutions designed for someone else.

The Access Gap

You're not losing on returns. You're losing on portfolio construction.

The difference isn't stock picking skill. It's access to asset classes, deal flow, and investment structures that aren't available at your scale.

Family offices have two critical advantages:

Patient capital. Unlike mutual funds facing quarterly redemption pressures, family offices can hold illiquid investments for decades. That staying power lets them capture the illiquidity premium—returns that compensate for not being able to sell quickly.

Superior deal access. Their networks grant co-investment opportunities alongside premier funds. They're not buying the same retail products wrapped in different packaging.

When 68% of family offices say private equity plays a "central role" in their strategy, and you can't replicate that allocation, you're not playing the same game.

TL;DR: The traditional model fails because advisors are trained for drawdown (not growth), you get retail products (not institutional access), and the AUM fee model requires 100% dependency (no partial partnerships). The industry has no construct for strategic partnership.

What Does This Actually Require?

The system works perfectly. You're not who it was designed for.

The traditional model assumes you want to delegate. You want to partner.

It assumes you're optimizing for preservation. You're optimizing for growth.

It assumes you need someone to "handle it." You need someone to educate you so YOU can handle it.

This isn't something a better advisor can fix. The constraints are structural:

Training optimized for a different client (drawdown, not growth)

Products designed for institutional scale (you're stuck with retail wrappers)

Incentives that require dependency (AUM model can't support partnership)

Capacity limits that make customization unprofitable

No construct for partial relationships (all-in or nothing)

The traditional advice isn't working for you—because it wasn't designed for you.

You need a different model entirely.

What You Actually Need

If the traditional model can't deliver what you want, what does?

You need education, not gatekeeping. Real frameworks for evaluating opportunities such as PE deals, real estate syndications, entity structures, tax strategies. Not "that's too risky for you" advice that protects the advisor's model.

You need to understand your options AND the risks. Full transparency on what works at your scale, what the trade-offs are, and how to make informed decisions. The smart money doesn't avoid complexity—they understand it.

You need aligned incentives. Partners who get paid for expertise and execution, not for keeping your capital locked in their AUM.

You need access to institutional-grade strategies. Not retail wrappers. The same playbook family offices use, scaled to your asset level.

And here's the critical piece: You need to know where to be passive and where to be active.

You don't have time to become a full-time investor. You shouldn't be researching municipal bond structures or filing entity paperwork yourself.

But you DO want control over:

Strategic allocation decisions

Which opportunities to pursue

How your wealth connects to your goals

When to deploy capital outside traditional markets

The model you need separates education from execution.

Learn the frameworks. Understand the options. Make the strategic decisions. Then hire specialists to execute within YOUR strategy—not theirs.

This is how family offices operate. The family sets the strategy. The team executes.

You're looking for the same structure, scaled to $1M-$30M.

TL;DR: You need education (not gatekeeping), aligned incentives (not AUM dependency), and institutional strategies scaled to your level. The model should separate education from execution—you make strategic decisions, specialists execute within your framework.

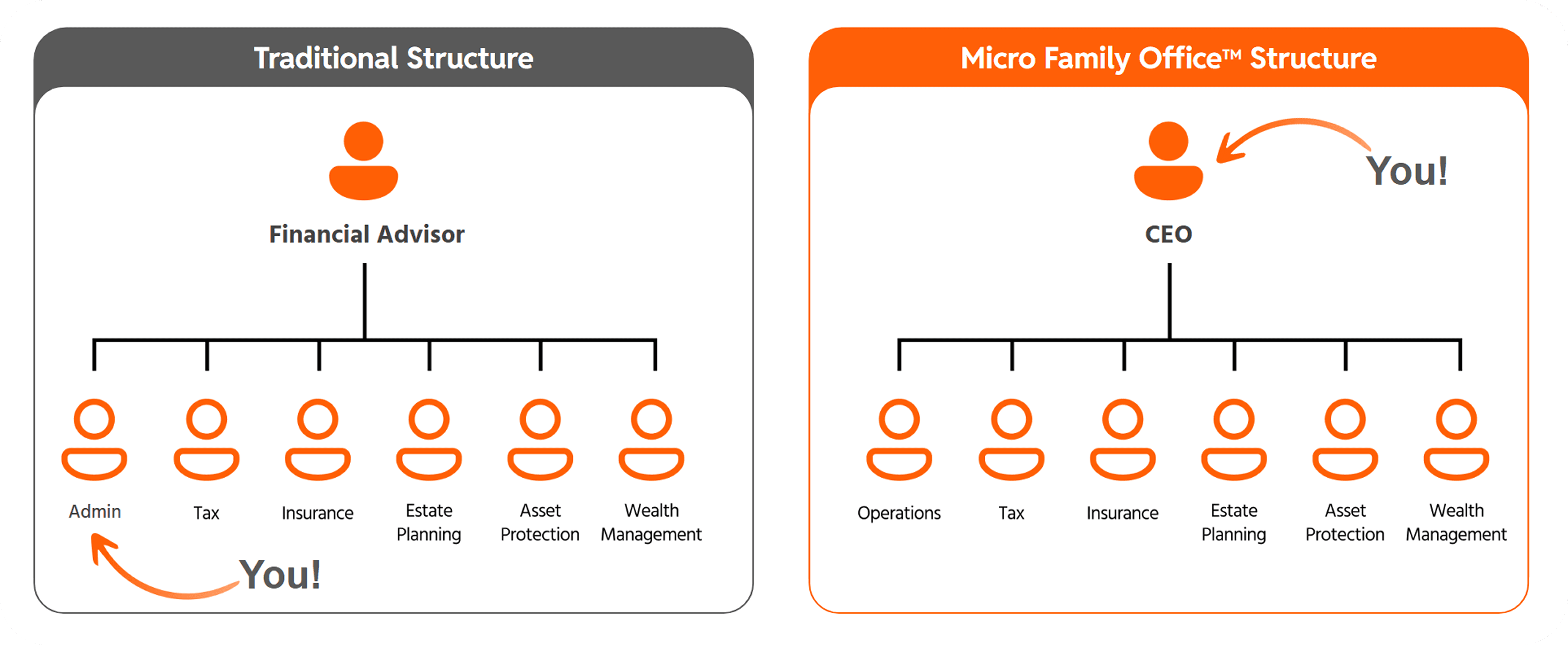

Why Did We Build WealthOps?

This gap, between what you need and what the industry offers, is why we built WealthOps.

We're not advisors. We don't manage assets. We don't sell financial products.

We're educators teaching the same frameworks family offices use, scaled for $1M-$30M portfolios.

The premise is straightforward: If you can run operations—and you can, that's how you built wealth—you can run a Micro Family Office. Same principles the ultra-wealthy use. Right-sized execution for your asset level.

What we teach:

The 7 MiFO Components — Vision, Structure, Protection, Process, Data, Advisory Partners, Governance. What every family office has. What you can build at your scale.

The Evergreen Model — Portfolio architecture designed for compounding indefinitely, not depleting over time. Income generation instead of drawdown.

The BUILD Framework — How to assess where you are (Portfolio Capability, MiFO Stage, Lifestyle Mode) and what to build at your level.

You become the Portfolio CEO. You architect the strategy. Advisors become specialist vendors—your CPA, your CTP, your bookkeeper, your estate attorney—executing within your framework.

Not dependents. Partners.

The shift: From "my advisor handles it" to "I run a wealth management business."

This isn't for everyone. If you want someone to handle everything, the traditional model still exists.

But if you want to apply the same operational mindset that built your wealth to your wealth? That's what this is designed for.

What Should You Do Next?

If you're in the Service Desert, you have options:

Option 1: Accept the template. Stay with traditional relationships, knowing you're getting preservation-focused advice and downstream products. Some people make peace with this.

Option 2: Go it alone. DIY everything. Learn tax code, entity structures, alternatives, estate planning. Possible, but expensive mistakes and high opportunity cost.

Option 3: Build your own infrastructure—and become the CEO.

This is the Micro Family Office approach. Same 7 components that run a $500M family office, scaled for $1M-$30M.

Want to learn more?

Subscribe: Managing Tech Millions on Substack

Watch: @managingtechmillions on YouTube

This is education, not advice. The wealth management landscape varies by individual circumstance. Learn the systems, then apply your judgment.

Let's keep building.

About the Author

Christopher Nelson is the founder of WealthOps and host of Managing Tech Millions. After three IPOs (Splunk, Yext, GitLab), he built his own Micro Family Office and has been managing a diversified portfolio generating $200K+ in annual cash flow for 4.5 years. He teaches high-net-worth professionals how to architect and operate their own wealth management infrastructure.

Sources

What Is the Financial Service Desert?

The Service Desert is the $1M-$30M wealth gap where no systematic solutions exist.

You're too complex for retail financial services. Robo-advisors can't handle equity compensation, alternative investments, or multi-entity tax strategy. Target-date funds weren't designed for someone building a real estate portfolio alongside their brokerage account.

You're too "small" for family office infrastructure. Single family offices require $100M minimum—some say $250M or more to justify the $1-2M annual operating cost. Multi-family offices set their floors at $25M-$100M and still treat you like a number.

The industry calls you "high net worth." Then it treats you like everyone else.

McKinsey defines the high-net-worth segment as $2M-$25M in investable assets. That's a massive range. And here's what the data shows: a $10M client paying $50,000 per year in advisory fees often receives identical treatment as a $2M client paying $16,000. Same templates. Same quarterly calls. Same recommendations.

You're paying three times as much for the same service.

TL;DR: The Service Desert is the $1M-$30M wealth gap where investors are too complex for retail services but too "small" for family office infrastructure. Despite paying $16K-$50K+ in fees annually, most receive identical template advice designed for retirement planning, not wealth building.

Why Does the Service Desert Miss What You Actually Want?

You didn't build $1M-$30M by being passive.

The wealth management industry assumes you need someone to "handle it for you." But you made this money by understanding how to build, evaluate opportunities, and make strategic decisions.

Now you want to apply that same mindset to your wealth.

The market is changing. Professionals with $1M-$30M aren't looking for someone to take over. They're looking for:

Control — Not blind delegation. You want to understand the strategy and own the decisions.

Strategic partnership — Not a relationship where moving capital outside the advisor's control feels like a betrayal.

Education to make more — Not gatekeeping disguised as "too risky for you."

This creates a fundamental mismatch. The traditional advisory model was built for a different client: someone nearing retirement who wants preservation. Someone who WANTS to delegate everything.

You're optimizing for growth. You want a partner, not a parent.

And the industry has no construct for that.

Here's why.

Why the Gap Exists

The Service Desert isn't a market failure. It's market design for a client that isn't you.

The Three Structural Failures:

The Service Desert exists because of three structural failures in the traditional wealth management model:

Training Mismatch: Advisors trained for retirement drawdown, not wealth building

Product Access Gap: Retail wrappers instead of institutional strategies

Incentive Misalignment: AUM model requires 100% dependency, no partial partnerships

Each failure has the same root cause: the model was designed for a different client.

Why Is Advisor Training Built for Drawdown, Not Growth?

Most financial advisors aren't trained to build wealth. They're trained for preservation and distribution.

What you want: Education on how to deploy capital strategically—PE deals, real estate syndications, business opportunities.

What they're trained for: 60/40 portfolios, target-date funds, and "don't outlive your money" drawdown strategies.

The origin of financial planning was selling products. That's still how many organizations operate today. You come in, you learn to sell. If you do well at sales, maybe at some point you get the opportunity to pursue your CFP certification and become an actual financial planner.

The result? There's a legal difference between advisors and salespeople. There's a standards difference. There's a training and education difference. But the industry doesn't discriminate in how those titles work. The person calling themselves your "wealth advisor" may have six weeks of product training, two weeks of sales training, and zero days on private equity, real estate syndication, or entity-based tax optimization.

Why? Because 65% of their clients are over 50, preparing for retirement. Their training is optimized for distribution, not accumulation. For preservation, not building.

You're trying to build. They're trained to help people draw down.

You're speaking different languages.

The model has no construct for: "Teach me how this works so I can make the decision" instead of "Let me handle this for you."

Why Don't You Get Access to Institutional Products?

What you want: Access to the same asset classes and deal flow that drive family office returns.

What you get: Retail wrappers of institutional strategies, with fees layered on top.

Here's where the gap becomes undeniable.

Family offices allocate 46-54% of their portfolios to alternative investments—private equity, venture capital, real estate, private credit. Their target return? 11%.

You? If you're lucky, you have 5-10% in alternatives, mostly through ETF wrappers or funds of funds with management fees layered on top. Your realistic target return? 7-8%.

That 3-4% difference compounds dramatically over decades.

But it gets worse. Private assets outperform public markets by 200-400 basis points annually. And 66% of family offices believe illiquidity—the very thing retail investors are told to avoid—actually boosts long-term returns.

The math is clear. The access is not.

Companies now stay private for 11 years before IPO. In the 1990s, it was six years. The value creation that used to happen in public markets—where you could participate—now happens before the company ever goes public. By the time you can buy, the biggest gains are already captured.

You're accredited. You legally qualify for private investments. But you get the retail versions of what actually builds wealth.

Why? The minimums.

Accredited investor ($1M net worth): Access to some private equity, but minimums of $250K-$1M per deal

Qualified Purchaser ($5M in investments): Access to better funds, 3(c)(7) structures, still limited deal flow

Family Office ($100M+): Co-investment alongside KKR, Blackstone, Bain Capital. Direct relationships with fund managers.

The investment opportunities that drive family office returns aren't available to you at the same scale, terms, or access points. You're playing on a different field.

The model has no construct for: Strategic allocation to alternatives alongside your managed account. Moving capital to a PE deal they can't access breaks their business model.

Why Do AUM Incentives Require Dependency?

What you want: A partner who helps you evaluate opportunities wherever they are—even if that means moving money outside their management.

What the model incentivizes: Keeping every dollar inside their AUM.

The AUM model—assets under management—creates structural conflicts that work against your interests.

Your advisor is paid a percentage of the assets they manage. Typically 1% annually. That means they're financially incentivized against anything that reduces your AUM:

Paying off your mortgage? Reduces AUM.

Investing in real estate they don't manage? Reduces AUM.

Moving money into private equity deals they can't access? Reduces AUM.

Using capital for business opportunities? Reduces AUM.

The strategies that build wealth often involve deploying capital outside your brokerage account. But every dollar that leaves is a dollar they stop earning on.

Fee-only doesn't mean conflict-free when the fee is tied to assets under management.

And as you move upmarket, seeking more sophisticated advice? The products get more complex—which means more fees layered in, more strings attached, more conflicts embedded. The exhaustion you feel isn't paranoia. Every interaction feels like a sales pitch because structurally, it is one.

The model has no construct for: Partial partnership. "I'll pay you for strategic advice and execution on X, but I'm also allocating to Y and Z on my own."

The business model requires 100% or nothing. You manage everything or you're not a client.

The Capacity Problem

Even good advisors can't solve this.

The average financial advisor manages 99-150 clients. That translates to roughly 4 hours per client per year—including all meetings, preparation, and follow-up.

Four hours.

For a $5M portfolio with equity compensation, real estate holdings, multiple entities, and complex tax considerations.

McKinsey projects the industry will face a shortage of roughly 100,000 advisors by 2034. The economics are pushing firms toward fewer clients with larger asset bases—not better service for anyone under $10M.

Rising costs mean rising minimums. Schwab raised their referral threshold from $500K to $2M. Private banks keep hiking their floors. The squeeze is on.

The result? You're either pushed down to robo-services that can't handle your complexity, or you're accepted as a client but served with template solutions designed for someone else.

The Access Gap

You're not losing on returns. You're losing on portfolio construction.

The difference isn't stock picking skill. It's access to asset classes, deal flow, and investment structures that aren't available at your scale.

Family offices have two critical advantages:

Patient capital. Unlike mutual funds facing quarterly redemption pressures, family offices can hold illiquid investments for decades. That staying power lets them capture the illiquidity premium—returns that compensate for not being able to sell quickly.

Superior deal access. Their networks grant co-investment opportunities alongside premier funds. They're not buying the same retail products wrapped in different packaging.

When 68% of family offices say private equity plays a "central role" in their strategy, and you can't replicate that allocation, you're not playing the same game.

TL;DR: The traditional model fails because advisors are trained for drawdown (not growth), you get retail products (not institutional access), and the AUM fee model requires 100% dependency (no partial partnerships). The industry has no construct for strategic partnership.

What Does This Actually Require?

The system works perfectly. You're not who it was designed for.

The traditional model assumes you want to delegate. You want to partner.

It assumes you're optimizing for preservation. You're optimizing for growth.

It assumes you need someone to "handle it." You need someone to educate you so YOU can handle it.

This isn't something a better advisor can fix. The constraints are structural:

Training optimized for a different client (drawdown, not growth)

Products designed for institutional scale (you're stuck with retail wrappers)

Incentives that require dependency (AUM model can't support partnership)

Capacity limits that make customization unprofitable

No construct for partial relationships (all-in or nothing)

The traditional advice isn't working for you—because it wasn't designed for you.

You need a different model entirely.

What You Actually Need

If the traditional model can't deliver what you want, what does?

You need education, not gatekeeping. Real frameworks for evaluating opportunities such as PE deals, real estate syndications, entity structures, tax strategies. Not "that's too risky for you" advice that protects the advisor's model.

You need to understand your options AND the risks. Full transparency on what works at your scale, what the trade-offs are, and how to make informed decisions. The smart money doesn't avoid complexity—they understand it.

You need aligned incentives. Partners who get paid for expertise and execution, not for keeping your capital locked in their AUM.

You need access to institutional-grade strategies. Not retail wrappers. The same playbook family offices use, scaled to your asset level.

And here's the critical piece: You need to know where to be passive and where to be active.

You don't have time to become a full-time investor. You shouldn't be researching municipal bond structures or filing entity paperwork yourself.

But you DO want control over:

Strategic allocation decisions

Which opportunities to pursue

How your wealth connects to your goals

When to deploy capital outside traditional markets

The model you need separates education from execution.

Learn the frameworks. Understand the options. Make the strategic decisions. Then hire specialists to execute within YOUR strategy—not theirs.

This is how family offices operate. The family sets the strategy. The team executes.

You're looking for the same structure, scaled to $1M-$30M.

TL;DR: You need education (not gatekeeping), aligned incentives (not AUM dependency), and institutional strategies scaled to your level. The model should separate education from execution—you make strategic decisions, specialists execute within your framework.

Why Did We Build WealthOps?

This gap, between what you need and what the industry offers, is why we built WealthOps.

We're not advisors. We don't manage assets. We don't sell financial products.

We're educators teaching the same frameworks family offices use, scaled for $1M-$30M portfolios.

The premise is straightforward: If you can run operations—and you can, that's how you built wealth—you can run a Micro Family Office. Same principles the ultra-wealthy use. Right-sized execution for your asset level.

What we teach:

The 7 MiFO Components — Vision, Structure, Protection, Process, Data, Advisory Partners, Governance. What every family office has. What you can build at your scale.

The Evergreen Model — Portfolio architecture designed for compounding indefinitely, not depleting over time. Income generation instead of drawdown.

The BUILD Framework — How to assess where you are (Portfolio Capability, MiFO Stage, Lifestyle Mode) and what to build at your level.

You become the Portfolio CEO. You architect the strategy. Advisors become specialist vendors—your CPA, your CTP, your bookkeeper, your estate attorney—executing within your framework.

Not dependents. Partners.

The shift: From "my advisor handles it" to "I run a wealth management business."

This isn't for everyone. If you want someone to handle everything, the traditional model still exists.

But if you want to apply the same operational mindset that built your wealth to your wealth? That's what this is designed for.

What Should You Do Next?

If you're in the Service Desert, you have options:

Option 1: Accept the template. Stay with traditional relationships, knowing you're getting preservation-focused advice and downstream products. Some people make peace with this.

Option 2: Go it alone. DIY everything. Learn tax code, entity structures, alternatives, estate planning. Possible, but expensive mistakes and high opportunity cost.

Option 3: Build your own infrastructure—and become the CEO.

This is the Micro Family Office approach. Same 7 components that run a $500M family office, scaled for $1M-$30M.

Want to learn more?

Subscribe: Managing Tech Millions on Substack

Watch: @managingtechmillions on YouTube

This is education, not advice. The wealth management landscape varies by individual circumstance. Learn the systems, then apply your judgment.

Let's keep building.

About the Author

Christopher Nelson is the founder of WealthOps and host of Managing Tech Millions. After three IPOs (Splunk, Yext, GitLab), he built his own Micro Family Office and has been managing a diversified portfolio generating $200K+ in annual cash flow for 4.5 years. He teaches high-net-worth professionals how to architect and operate their own wealth management infrastructure.

Sources

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.

Next Steps

Want to attend our next live workshop? Complete the application on this page to join us.

Want weekly frameworks? Subscribe to Managing Tech Millions newsletter.

Prefer video? Check out the Managing Tech Millions YouTube channel.